Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

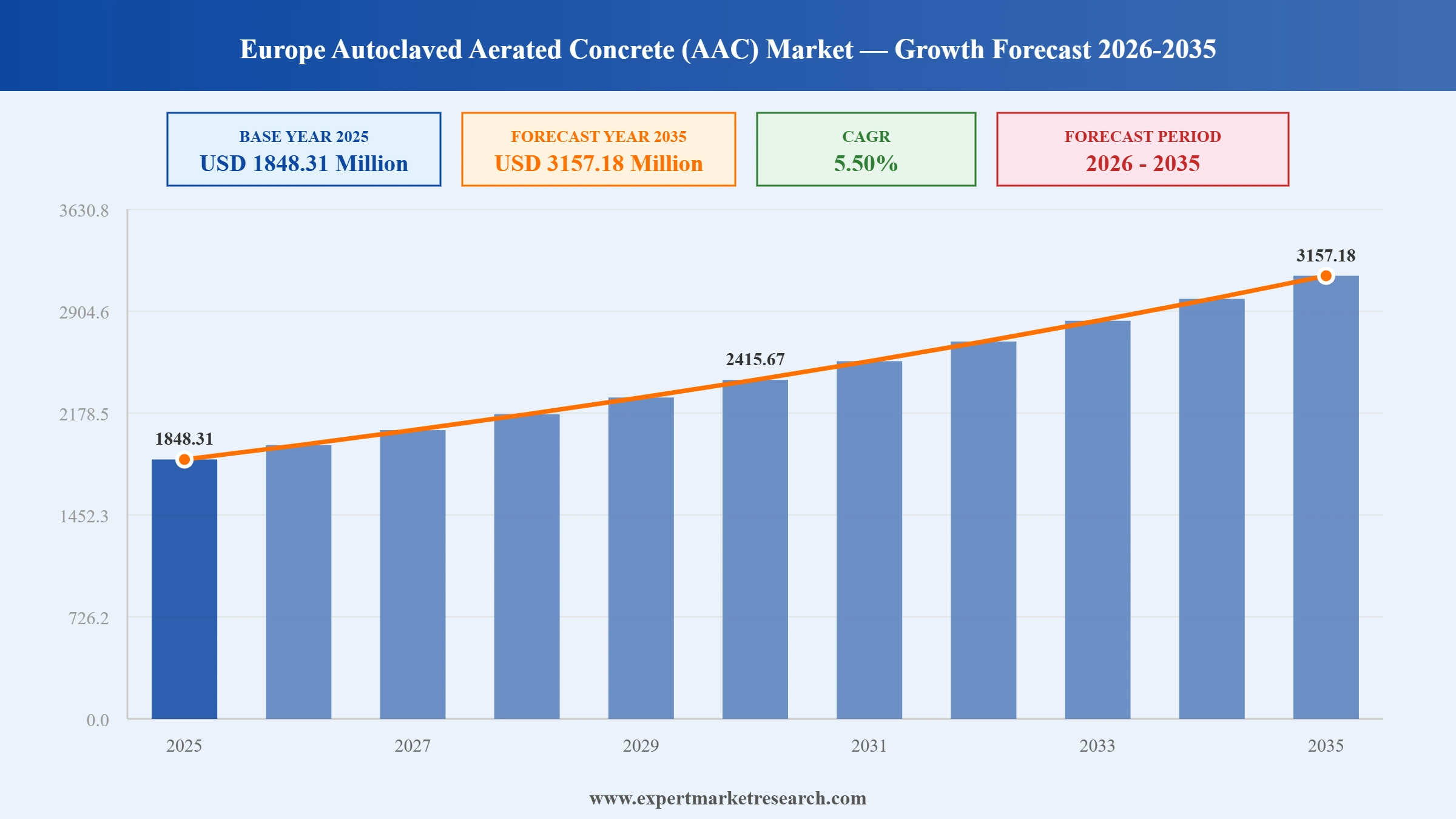

Europe Autoclaved Aerated Concrete (AAC) Market reached a value of USD 1848.31 Million in 2025 and is set to grow at a CAGR of around 5.50% through 2026-2035. Increasing renovation activities, a rising inclination towards sustainable construction, and the cost savings and energy efficiency provided by AAC products are reinforcing growth momentum. The market is on track to reach USD 3157.18 Million by 2035. Lightweight and thermally efficient walling, tightening EU energy-performance standards, the growth of prefabricated and modular systems, and consolidation among leading producers are fuelling the Europe autoclaved aerated concrete (AAC) market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Europe autoclaved aerated concrete (AAC) market is being shaped by major consolidation among walling producers, the EU drive for energy-efficient and sustainable construction, the growth of prefabricated systems, and challenging residential demand in key markets such as Germany.

In June 2026, Holcim completed its acquisition of Xella, the European AAC and walling leader behind Ytong, Hebel, Silka, and Multipor. The deal, cleared by the European Commission subject to divesting an AAC blocks plant in Romania, expands Holcim's sustainable building solutions portfolio.

In March 2026, H+H International approved its 2025 results, with revenue of around DKK 2.7 billion and improved EBIT before special items, led by the United Kingdom, Poland, and Switzerland. Its German AAC business remained loss-making and under continued restructuring amid weak residential demand.

In October 2025, Holcim agreed to acquire Xella from Lone Star Funds for EUR 1.85 billion, targeting Europe's energy-efficient refurbishment and walling market. The transaction underscored cement groups' strategic shift into higher-value, sustainable building solutions, including AAC systems.

In April 2025, Solbet increased its shareholding in H+H International to around 25%, deepening ties between two leading European AAC producers. The move highlighted ongoing strategic positioning and consolidation dynamics within the European autoclaved aerated concrete market.

Sustainable construction anchors the Europe AAC market. Tightening EU energy-performance standards, decarbonisation targets, and demand for thermally efficient, fire-resistant walling are sustaining AAC adoption, as producers advance low-carbon formulations and circular, resource-efficient manufacturing across the region.

Renovation and refurbishment are key drivers of the Europe AAC market. Europe's large, ageing building stock and substantial refurbishment economy are lifting demand for energy-efficient walling and insulation, supported by policy-led incentives and the push for higher-performance, lower-carbon buildings.

Prefabrication is reshaping the Europe AAC market. Prefabricated Ytong and Hebel panels, modular systems, and digital tools such as BIM-linked planning accelerate build schedules and reduce on-site labour and waste, expanding the role of panelised AAC in modern construction.

Consolidation is reshaping the Europe AAC market. Cement and building-materials groups are acquiring walling specialists, exemplified by Holcim's purchase of Xella, while family-owned producers reach succession points, intensifying cross-border competition and integration across the value chain.

Cost and operational pressures shape the Europe AAC market. Energy represents a large share of AAC production cost, prompting efficiency and fuel-switching investments, while weak residential demand in markets such as Germany contrasts with resilience in the United Kingdom and Poland.

The report of Expert Market Research's titled “Europe Autoclaved Aerated Concrete (AAC) Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

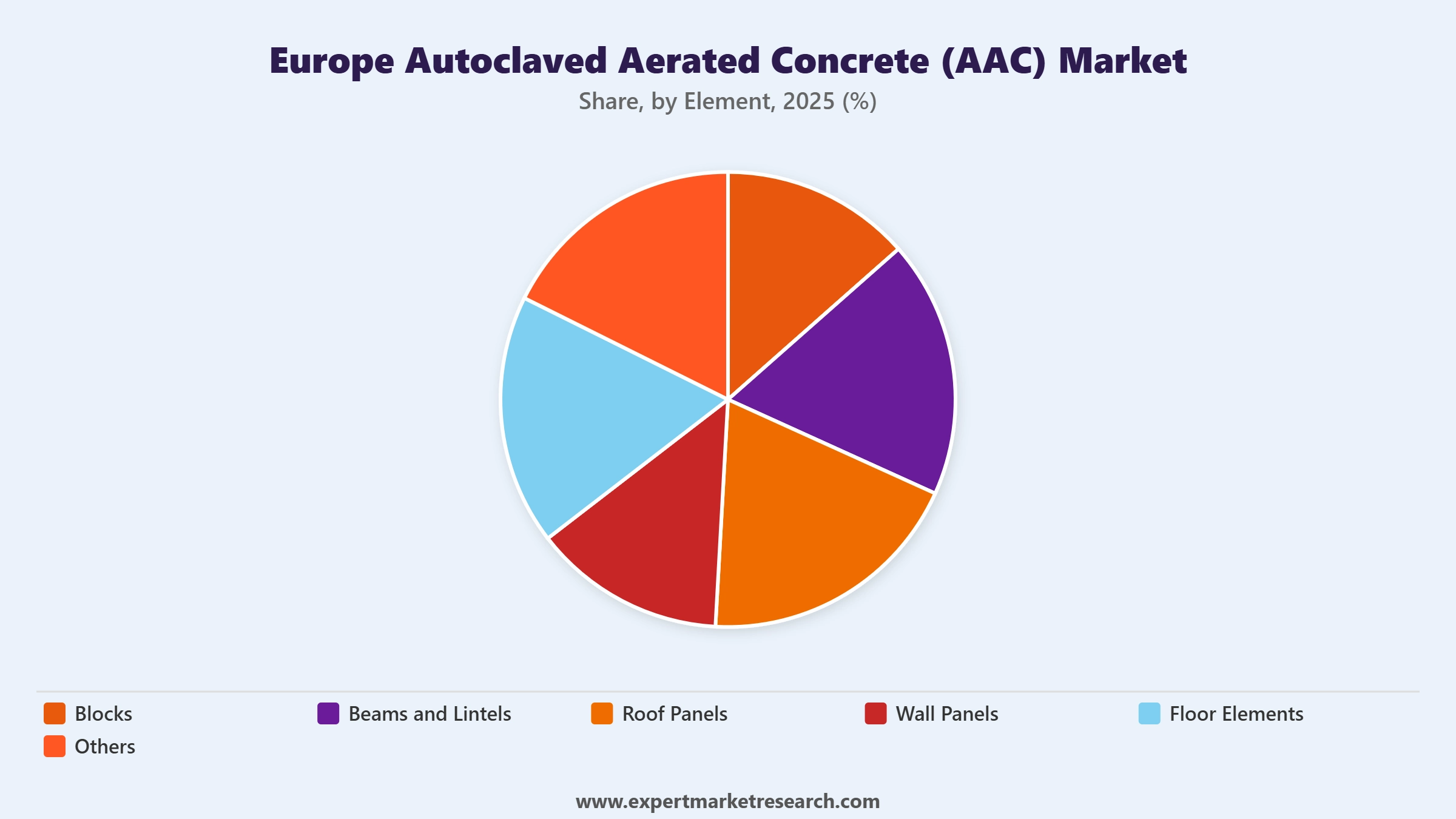

Market Breakup by Element

Key Insight: Blocks account for the largest share of the Europe AAC market, valued for their light weight, ease of installation, and thermal efficiency in residential and mid-rise construction. Wall, roof, and floor panels are growing through prefabrication, while beams and lintels provide supporting structural elements across building applications.

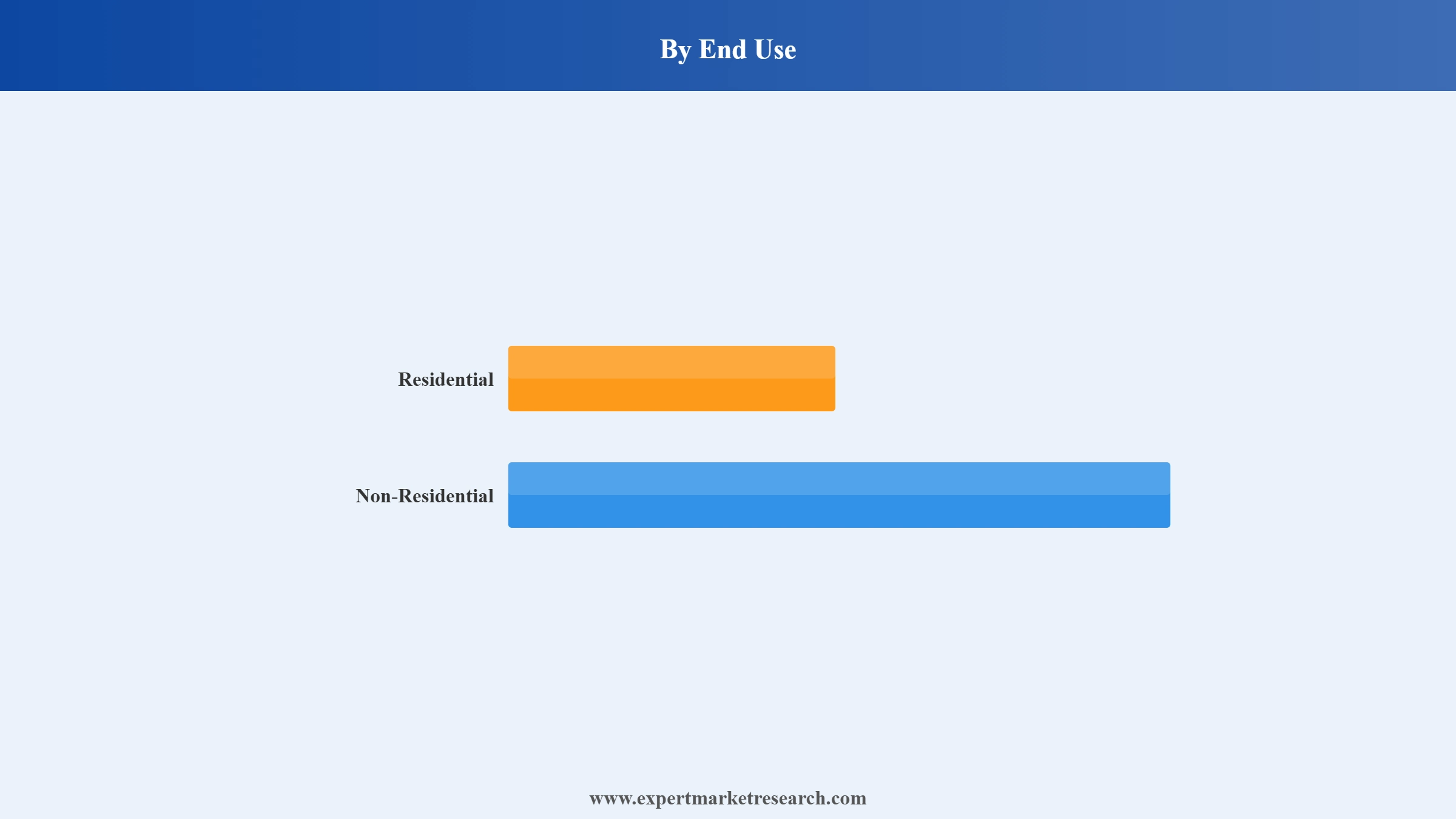

Market Breakup by End Use

Key Insight: Residential construction accounts for the largest share of the Europe AAC market, supported by new housing and energy-efficient renovation. The non-residential segment, spanning commercial, industrial, and government projects, is the fastest-growing, driven by infrastructure investment and rising demand for thermally efficient, durable buildings.

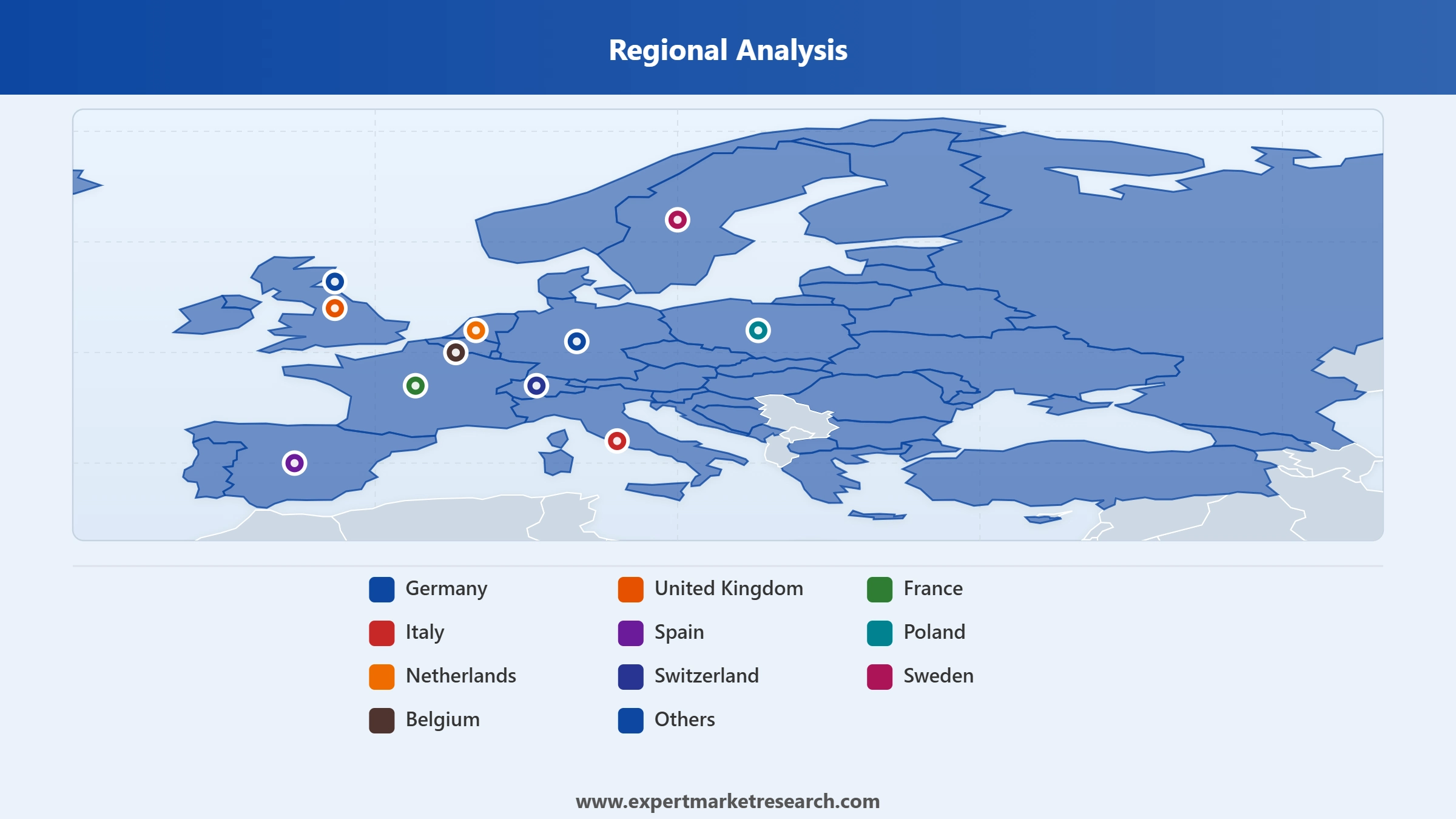

Market Breakup by Country

Key Insight: Germany dominates the Europe AAC market, anchored by a large AAC base and leading producers, while Poland is a major and fast-growing market. The United Kingdom, France, Italy, and Spain hold significant shares, and the Nordic and Benelux markets remain steady on energy-efficiency demand.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Element, Blocks dominate the market while panels grow through prefabrication

Blocks hold the dominant share of the Europe AAC market, valued for being lightweight, easy to cut and install, and highly thermally efficient. AAC blocks, far lighter than traditional bricks, suit residential and mid-rise walling, offering fire resistance and insulation that align with the region's energy-efficiency and sustainability priorities.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Wall, roof, and floor panels are growing fastest, driven by prefabrication and modular construction. Prefabricated Ytong and Hebel systems, supported by digital, BIM-linked planning, accelerate build schedules and reduce labour, while beams and lintels add structural versatility, broadening AAC use across the Europe autoclaved aerated concrete market.

By End Use, Residential leads the market while Non-Residential grows the fastest

Residential construction leads the Europe AAC market, underpinned by new housing and a large energy-efficient renovation economy. AAC's thermal performance, fire resistance, and ease of use make it well suited to homes and mid-rise buildings, with refurbishment of ageing stock providing a stable, policy-supported demand base across the region.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The non-residential segment, spanning commercial, industrial, and government construction, is the fastest-growing. Demand is supported by infrastructure investment and the lifecycle cost and energy-efficiency benefits of AAC in offices, factories, and public buildings, steadily broadening its share within the Europe autoclaved aerated concrete market.

Germany dominates while Poland is a key and fast-growing market

Germany dominates the Europe AAC market, anchored by a deep tradition of AAC use, leading producers such as Xella and H+H, and strong demand for energy-efficient walling. Despite a challenging residential construction environment in recent years, Germany remains the region's largest market, supported by renovation and stringent energy-performance standards.

Poland is a key and fast-growing market, benefiting from strong construction fundamentals and well-established AAC adoption. The United Kingdom, France, Italy, and Spain hold significant shares, while the Netherlands, Switzerland, Sweden, and Belgium remain steady, collectively reinforcing the depth and diversity of the Europe autoclaved aerated concrete market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The Europe AAC market is moderately consolidated, led by specialist walling producers and diversified building-materials groups. Xella and H+H International anchor the AAC segment, alongside CRH and Holcim, which is integrating Xella, with regional specialists such as Bauroc and Solbet strengthening competition across the value chain.

Competition centres on product performance, energy efficiency, prefabrication, geographic footprint, and sustainability. Leading players invest in low-carbon production, panelised and modular systems, digital planning, and selective acquisitions, while navigating weak residential demand in some markets and tightening EU regulation that increasingly favours thermally efficient, lower-carbon walling.

Headquartered in Duisburg, Germany, Xella is the world's largest manufacturer of autoclaved aerated concrete and calcium silicate, with brands including Ytong, Hebel, Silka, and Multipor. It offers prefabricated AAC systems and digital BIM-linked services, and was acquired by Holcim in 2026, operating across more than 20 European markets.

Headquartered in Copenhagen, Denmark, and listed on Nasdaq Copenhagen, H+H International is a leading European producer of AAC (aircrete) and calcium silicate wall building materials. With factories across Northern and Central Europe, it holds strong positions in markets such as the United Kingdom, Poland, and Switzerland.

Headquartered in Dublin, Ireland, CRH is a leading global building materials company offering cement, aggregates, and a broad range of building products and solutions. Through its extensive European operations and product portfolio, it participates in the walling and construction materials markets relevant to AAC.

Headquartered in Switzerland, Holcim is a leading global building materials and solutions company focused on sustainable construction. Through its building solutions strategy and 2026 acquisition of Xella, it has significantly strengthened its position in the European AAC and walling market, including energy-efficient refurbishment.

Other key players in the market include Bauroc AS, SOLBET Spółka z o.o., and others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Our full report for 2026-2035 provides the demand analysis, element, end-use, and country segmentation, and competitive benchmarking to navigate the Europe autoclaved aerated concrete (AAC) market with confidence. Reach out to our team to access the complete report or request a customised version.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the market reached an approximate value of USD 1848.31 Million.

The market is projected to grow at a CAGR of 5.50% between 2026 and 2035.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 3157.18 Million by 2035.

The elements include blocks, floor elements, wall panels, beams and lintels, roof panels, and others.

The key countries analysed in the market report are the United Kingdom, Germany, France, Italy, Spain, Poland, the Netherlands, Switzerland, Sweden, Belgium, and others.

The end uses include residential and non-residential.

The factors driving the market growth are increasing renovation activities, rising inclination towards sustainable construction, and cost savings provided by AAC products, among others.

The key players in the market include H+H International A/S, CRH plc, Bauroc AS, Xella International GmbH, Holcim Limited, and Solbet Sp. z o.o., among others.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Element |

|

| Breakup by End Use |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.