Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

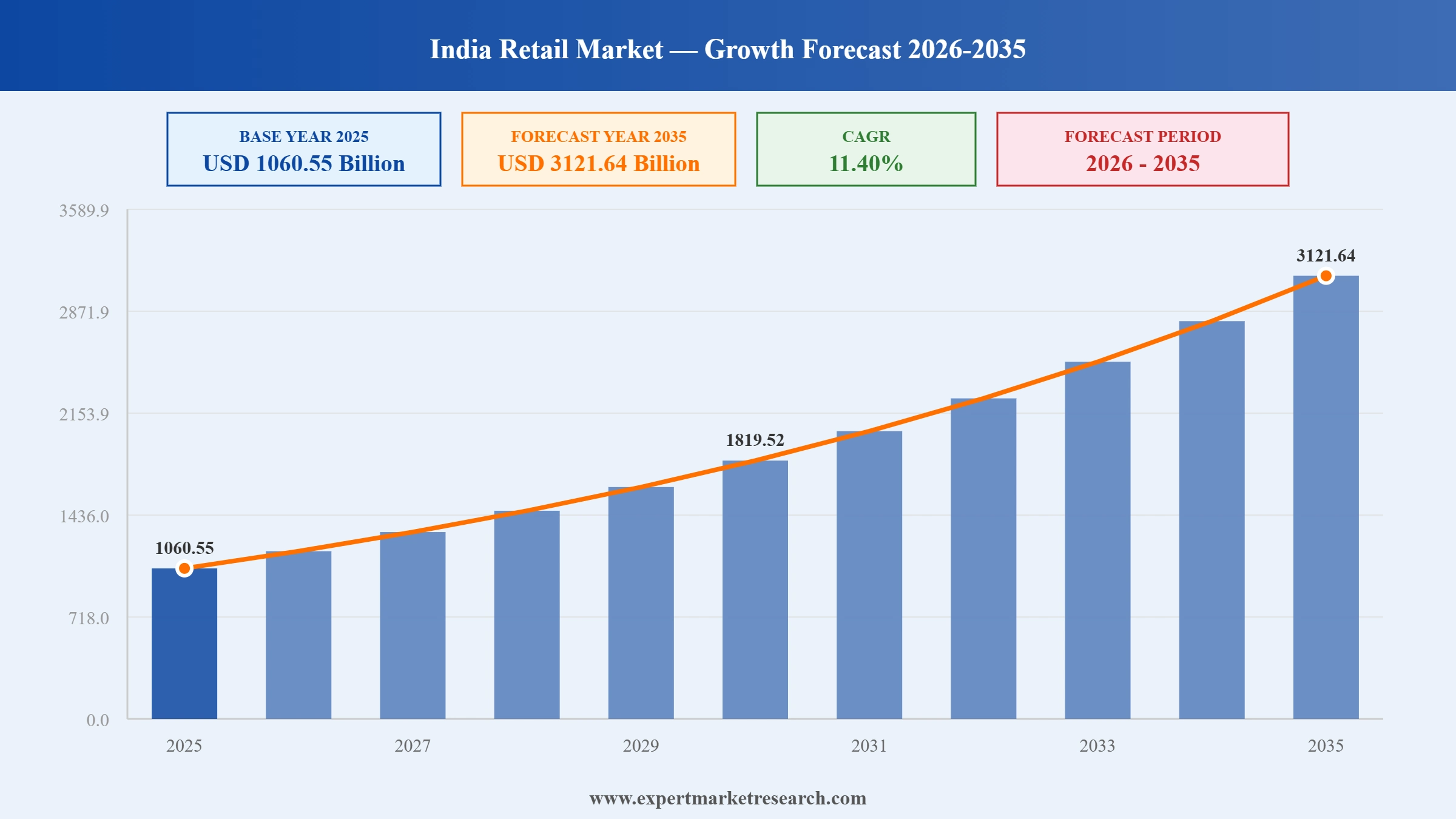

The India retail market size USD 1060.55 Billion in 2025. The market is expected to grow at a CAGR of 11.40% during the forecast period of 2026-2035 to reach a value of USD 3121.64 Billion by 2035. Tier II and III cities' increasing disposable incomes and digital exposure are driving demand for mid-format retail stores, enabling brands to expand beyond metro cities with cost-effective, experience-driven outlets and localised assortments.

Supermarkets account for nearly 12%-15% of all consumer goods sales in India.

Kirana stores account for nearly 75%-78% of all consumer goods sales in India.

Omnichannel retail is expected to remain popular among Indian consumers over the forecast period.

Reliance Retail Ventures reported full-year fiscal 2026 revenue of Rs 3.70 lakh crore, an 11.83% increase year-on-year, with profit after tax climbing to Rs 13,842 crore. The Press Trust of India highlighted that store count crossed 20,000 outlets while registered customer base expanded 10.9% to 387 million and transactions grew 38.8% to 1.93 billion. The performance reaffirms Reliance's leadership in India's organized retail expansion drive.

The Retailers Association of India business survey reported retail sales growth of 10% year-on-year in March 2026, capping fiscal 2026 with broad-based momentum. West and North India led at 11%, while food and grocery rose 14%, apparel 13%, jewellery 12%, and quick-service restaurants 11%. Consumer durables lagged with only 1% growth. The Hindu Business Line covered the survey, highlighting steady consumption resilience despite inflationary pressures and regional weather disruptions.

The Indian market is undergoing a structural transition, notably driven by the rising dominance of phygital commerce, an integration of digital and physical retail channels. Majority of the organised retailers have adopted hybrid models to cater to Tier II and III cities in India. As per the India retail market analysis, with smartphone penetration surpassing 880 million and UPI transactions crossing INR 18.68 billion in May 2025, the shift has become deeply infrastructural.

Meanwhile, government-backed initiatives are fuelling formalisation across sectors. The Open Network for Digital Commerce (ONDC), launched by DPIIT, onboarded over 3,70,000 sellers by March 2024, targeting small traders in Tier IV and rural belts. This is pushing the democratisation of retail accessibility. With integrations across logistics, payment gateways, and last-mile delivery platforms, ONDC is enabling even single-store retailers to reach pan-India consumers. The initiative also encourages fair pricing, enhances seller autonomy, and reduces dependency on large e-commerce intermediaries, boosting the India retail market growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The National Stock Exchange of India (NSE) announced on April 27 that its registered investor base crossed the 130 million mark. This milestone, reached just seven months after hitting 120 million, highlights an accelerating pace of retail participation in India's capital markets as digital platforms continue to simplify access for individual investors.

Official data released on April 13 showed India’s retail inflation stood at 3.40% in March 2026, based on the revised Consumer Price Index series. While food inflation rose slightly to 3.87%, a moderation in the prices of essentials like onions and pulses helped maintain overall stability, though high inflation persisted in the jewelry and precious metals segments.

India's retail inflation accelerated to an 11-month high of 3.21% in February 2026, driven primarily by a rebound in the Consumer Food Price Index to 3.47%. The personal care segment recorded a high inflation rate of 19.6%, largely fueled by a 48.16% year-on-year surge in the prices of gold, diamond, and platinum jewelry.

Retail inflation rose to 2.75% in January 2026, marking the first time in five months that the rate returned within the Reserve Bank of India’s 2–6% target band. The Ministry of Statistics highlighted that the weight of food items in the CPI basket has been reduced from 45.86% to 36.75% in the revised 2024-base series.

India’s next wave of retail growth is largely noticed in hybrid outlets in Bhopal, Indore, and Bhubaneswar. According to the India retail market analysis, 60-65% of Indian consumers prefer physical store experience seamlessly blended with the digital conveniences of a website. Players like Zudio and DMart Ready are opening small-footprint, digitally integrated stores in non-metro cities, leveraging localised logistics. The Government’s Digital India programme is also expected to facilitate cities with a population of over 1 million and tourist centres with public wi-fi hotspots to promote digital cities, strengthening rural digital infrastructure.

Supported by the Startup India initiative and SIDBI's digital acceleration fund, MSMEs are investing in cloud-based POS, inventory management and CRM tools, redefining the India retail market trends. With retail-technology becoming affordable, wholesalers and distributors targeting India must realign sales strategy with digitally savvy retailers. Brands like Bikayi and OkCredit that plug into MSME technology ecosystems are witnessing faster turnaround in B2B payments and better data-backed forecasting.

The luxury retail market in India is no longer confined to Delhi or Mumbai. Cities like Surat, Kochi, and Chandigarh now account for significant shares of the total high-value retail sales. International brands like Montblanc and Coach are opening ‘studio-format’ stores in urban Tier II malls. The Indian government’s Ease of Doing Business push has also reduced foreign retail entry timelines. B2B players in interior décor, retail leasing, and supply chain should monitor this trend closely as premium category expansion drives higher-margin contracts.

Backed by the INR 10,000 crore allocation under the Gati Shakti Yojana, retail-linked warehousing capacity is expected to be increased by 41 million sq. ft between 2024 to 2028. Urban freight corridors in Delhi NCR, Bengaluru, and Hyderabad are reducing last-mile transit time, accelerating further demand in the India retail market. Modern retailers now demand “just-in-time” delivery contracts, creating opportunity for B2B logistics, cold chain and automation vendors. Fulfilment centres that integrate with real-time inventory platforms are becoming essential. B2B buyers must adapt to supply-side pressure for shorter cycles and flexible handling.

India’s Gen Z and millennial consumers crave retail experiences over mere transactions. Retail chains like The White Crow and Phoenix Marketcity are merging co-working spaces with retail zones, supported by FDI-friendly real estate reforms. The Indian government’s Smart Cities Mission is prioritising mixed-use retail clusters, across Nagpur and Rajkot, accelerating India retail market growth. For B2B real estate developers and experience technology integrators, these hybrid formats demand next-gen lighting, air quality technology, and interactive digital signage, transforming the traditional buyer-seller ecosystem into multi-sensory interaction zones.

The Expert Market Research's report titled “India Retail Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

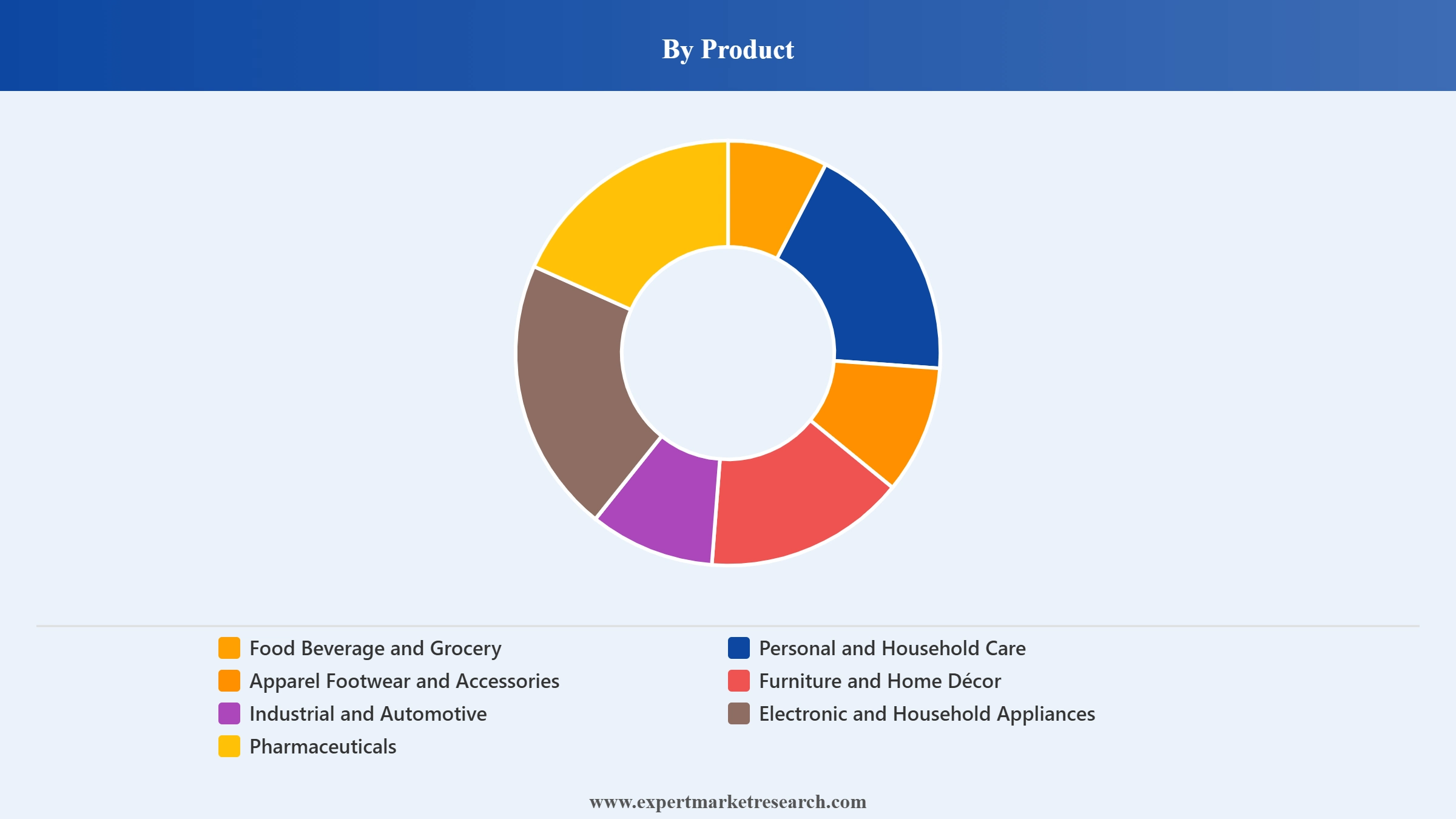

Market Breakup by Product

Key Insight: Food and grocery retain dominance in the India retail market dynamics due to daily demand, however, tech-powered categories like electronics and pharmaceuticals are growing at a fast pace. Apparel gains from hybrid fashion retail. Furniture benefits from urban migration, while automotive and industrial supplies are increasingly shifting online via verticalised B2B platforms. Personal care, driven by influencer commerce, is seeing a major traction from Gen Z buyers across platforms.

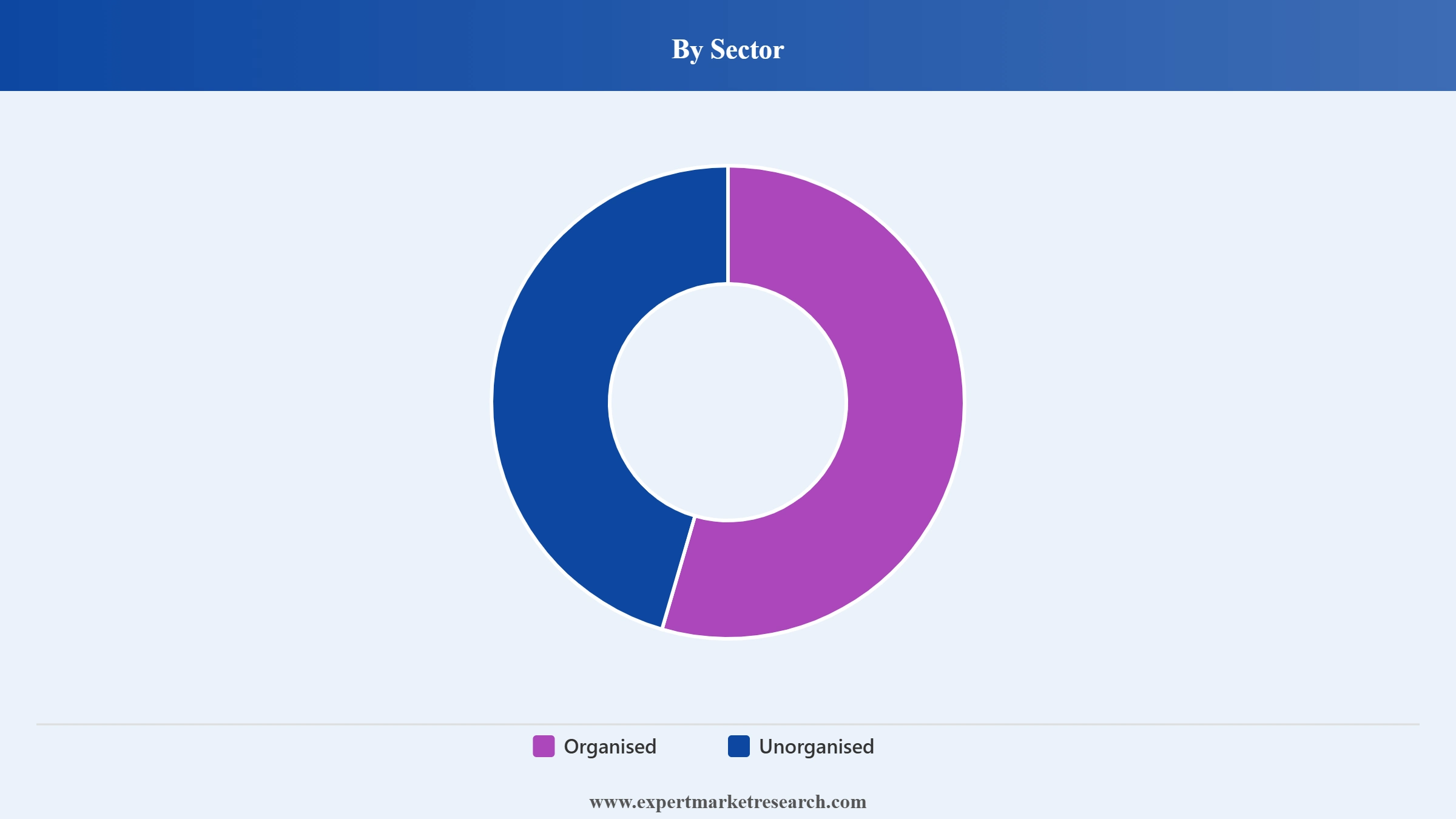

Market Breakup by Sector

Key Insight: The organised category largely drives the India retail market value through technology and logistics, while the unorganised sector commands volume and reach. Kiranas are digitally onboarding and demanding supplier-grade services. Meanwhile, modern retailers are moving into semi-urban belts to tap into new demand clusters. The evolving landscape requires adaptive B2B models including smart catalogues, modular warehousing, and API-linked distribution networks.

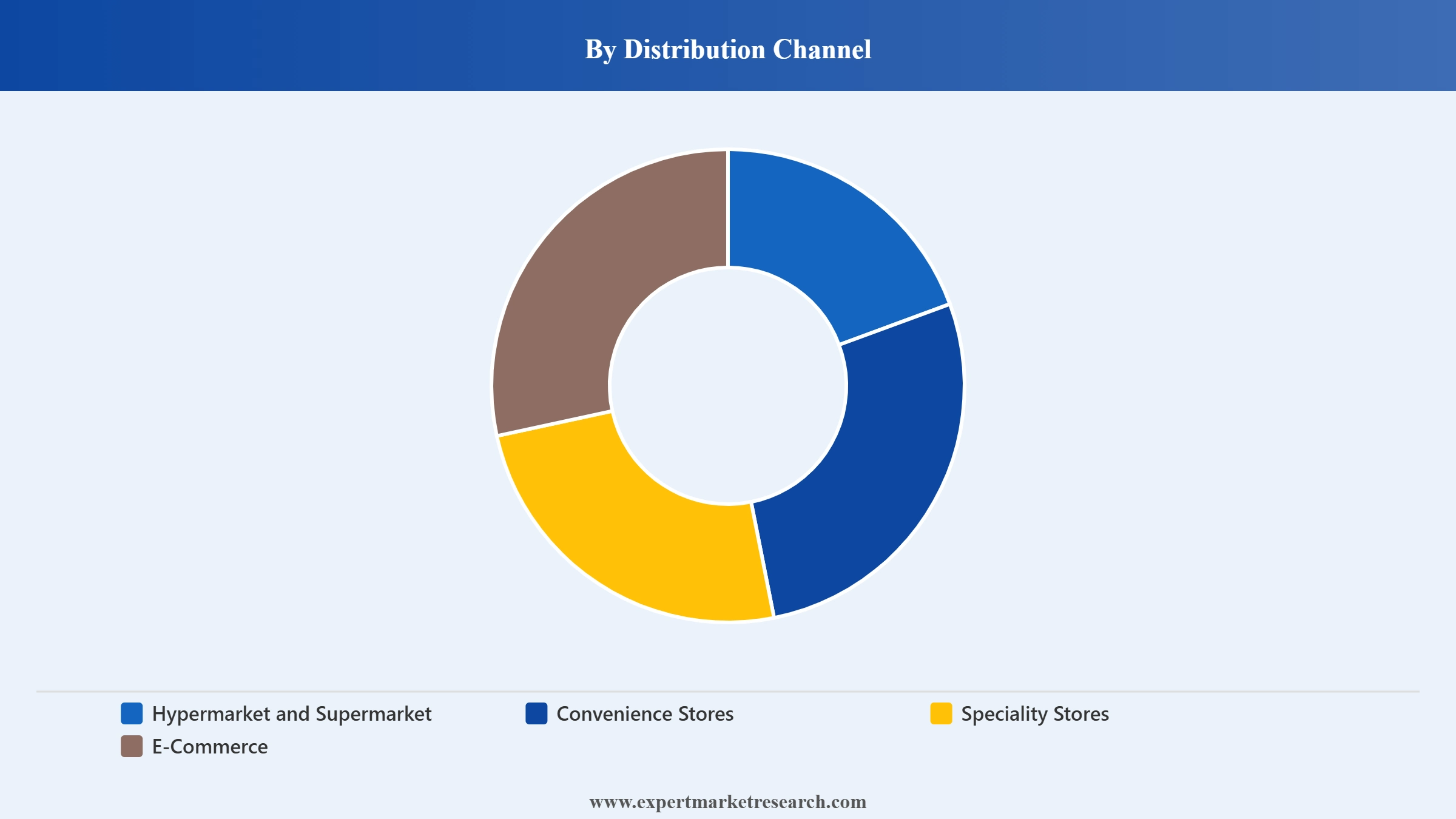

Market Breakup by Distribution Channel

Key Insight: E-commerce leads the India retail market owing to its digital ease and vast reach, while speciality stores grow by offering focused, experience-led shopping. Hypermarkets continue driving bulk sales across cities, and convenience stores gain traction through proximity and quicker turnaround. Other formats, like department chains, continue to be relevant, especially among legacy urban shoppers seeking multi-category access under one roof.

Market Breakup by Region

Key Insight: North India maintains its lead in the market with its dense retail infrastructure and metro-driven consumption hubs. East and Central India are quickly emerging, backed by rising income levels and improved connectivity. The South India retail industry stands out for its high digital adoption and tech-integrated retail formats, while West India offers consistent demand across both value and premium categories.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By product, food, beverage, and grocery maintains market dominance amid rising daily essentials demand

Food, beverages, and grocery continue to dominate the Indian market. This category benefits from habitual consumption, low price elasticity, and daily repeat purchases. Hyperlocal fulfilment has become the new retail currency as platforms like Reliance Smart and BigBasket now rely on real-time inventory dashboards and micro-warehousing to meet instant delivery demands. B2B suppliers are increasingly tailoring bulk SKUs and bundled products to suit this expanding digital shelf space.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Electronics and appliances are registering the fastest growth in the India retail market, fuelled by EMI-led UPI adoption and rising demand for smart gadgets. Direct-to-consumer brands like boAt, Noise, and Xiaomi are scaling via blended retail formats, combining pop-up stores with mobile-led platforms. Moreover, regional OEM partnerships and GST simplification have eased inter-state movement of high-value stock. Urban Tier II cities are turning into electronics hubs, supported by last-mile logistics startups.

By sector, organised retail leads the market with smart infrastructure and GST-backed efficiency

Organised retail continues to expand its retail market share in India powered by technology. Retail giants like Tata Neu and Reliance Retail are embedding AI into POS, inventory management, and loyalty solutions to personalise customer journeys. GST implementation has harmonised tax filing and vendor onboarding, reducing delays and boosting cross-state supply chain fluidity. From predictive stock replenishment to RFID-based inventory audits, organised players are setting new benchmarks for efficiency.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Despite its informal structure, the unorganised retail category commands significant shares of the Indian market. With ONDC, platforms like Udaan, and fintech enablers such as OkCredit and Khatabook, several kirana stores are now running semi-digital operations. Government schemes like PM-SVANidhi and Mudra Yojana have provided over INR 24,000 crore in micro-loans to small vendors, empowering them to upgrade infrastructure, digitise inventories, and expand assortments.

By distribution channel, e-commerce held the largest share of the market due to digital penetration

E-commerce emerges to be the dominant channel, boosting the India retail market revenue, largely due to its wide reach, convenience, and seamless integration with mobile payment systems. Increasing smartphone usage, real-time delivery, and regional warehousing make e-commerce accessible to rural and Tier II markets. Leading platforms like Flipkart and Amazon now offer express delivery options, enabled by AI-backed inventory and delivery management systems. ONDC is also boosting small sellers’ access to pan-India demand, accelerating digital marketplace growth.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Speciality stores are also contributing to the India retail demand forecast as consumers seek curated experiences and category expertise. From ethnic wear to organic food, these stores offer value through personalised services, brand storytelling, and hyperlocal sourcing. Urban millennials are shifting towards niche retail brands over generic ones, fuelling this category’s growth. Independent speciality chains and premium global brands are exploring small-format stores across metros and mini-metro cities. Supported by easier licensing norms and mall partnerships, these stores are building loyal customer bases.

North India held the largest share of the market due to dense urbanisation

The ongoing dominance of the North India retail market is particularly driven by Delhi NCR, Chandigarh, and Lucknow. The region benefits from a high density of malls, retail parks, and metro connectivity, offering seamless access to a large consumer base. With higher disposable incomes and a stronghold of organised players, North India presents a robust retail ecosystem. Government-backed smart city investments and improving logistics infrastructure have made the region favourable for quick commerce and fulfilment solutions, drawing attention from national and international B2B suppliers and distributors.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The east and central region is witnessing remarkable growth in the India retail market due to improved infrastructure and digital connectivity. Retail giants are expanding footprints in cities like Ranchi, Bhubaneswar, and Raipur, responding to rising income levels and aspirational consumption. Government incentives under schemes like UDAN and industrial corridor projects are connecting remote regions to retail supply chains. The entry of retail warehousing and regional fulfilment centres is making supply more efficient.

The country’s retail landscape is becoming more innovation centric. Leading India retail market players are now prioritising agility in inventory, seamless omnichannel experiences, and micro-fulfilment models. With ONDC unlocking participation for small traders, companies are racing to integrate their backend with government-supported networks. Partnerships with last-mile startups, investments into dark stores, and AI-driven consumer analytics are key focus areas.

India retail companies are also leveraging experiential zones, loyalty ecosystems, and co-branded digital finance to deepen engagement. For B2B players, this ecosystem demands smarter logistics, interoperable tech systems, and adaptive product design. Opportunities lie in predictive stocking, automated warehousing, and retailer-supplier financing platforms. As urban saturation sets in, regional penetration and rural digitisation are next frontiers. Brands that localise assortments while maintaining scalable backend integration will be best positioned to capture the evolving landscape.

Established in 1958, headquartered in Mumbai, Reliance dominates retail via Reliance Retail and JioMart. It’s integrating kiranas into its supply chain using JioPoS and has invested in smart fulfilment tech, AI-driven stock predictions, and rural last-mile delivery models. Its partnerships with Meta and ONDC enable seamless integration for smaller sellers.

Formed in 1857 and based in Mumbai, Aditya Birla operates through ABFRL and More Retail. It focuses on premium fashion, value retail, and omnichannel infrastructure. The company is expanding smart stores under brands like Pantaloons and plans deeper integration with loyalty platforms and digital wallets. It leverages predictive analytics to optimise inventory and enhance customer experience.

Established in 2002 and headquartered in Mumbai, DMart is known for its lean cost model and strong in-house logistics. The company’s growing DMart Ready app brings online reach without compromising its core discount model. It uses private labels strategically and maintains tight control on vendor margins and inventory cycles.

Founded in 1917 and based in Mumbai, Tata Group manages retail via Tata Consumer, Croma, and Tata Neu. It leverages data through Tata Digital to personalise offerings across verticals. From groceries to electronics, it blends brand variety with tech-backed shopping experiences. Tata Neu connects cross-brand loyalty into a single ecosystem. With acquisitions like BigBasket and 1mg, Tata is building an end-to-end consumer retail network, giving B2B partners scale with stability.

Other key players in the market are Vijay Sales (INDIA) Private Limited, V--Mart Retail Ltd., K Raheja Corp. (Shoppers Stop Ltd.), Landmark Group, V2Retail Ltd., and RP Sanjiv Goenka Group (Spencer’s Retail Limited), among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Explore the latest trends shaping the India retail market 2026-2035 with our in-depth report. Gain strategic insights, future forecasts, and key market developments that can help you stay competitive. Download a free sample report or contact our team for customised consultation on India retail market trends 2026.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India retail market reached an approximate value of USD 1060.55 Billion.

The market is projected to grow at a CAGR of 11.40% between 2026 and 2035.

The market is assessed to witness a healthy growth in the forecast period to reach around USD 3121.64 Billion in 2035.

The different distribution channels in the market include hypermarket and supermarket, convenience stores, speciality stores, and e-commerce, among others.

The major sectors in the market include organised and unorganised.

The different products considered in the market report are food, beverage, and grocery, personal and household care, apparel, footwear, and accessories, furniture and home décor, industrial and automotive, electronic and household appliances, and pharmaceuticals, among others.

The major regions in the market include North India, East and Central India, West India, and South India.

The key market players are Reliance Industries Limited, Aditya Birla Group, Avenue Supermarts Limited (DMart), Tata Sons Private Limited, Vijay Sales (INDIA) Private Limited, V--Mart Retail Ltd., K Raheja Corp. (Shoppers Stop Ltd.), Landmark Group, V2Retail Ltd., and RP Sanjiv Goenka Group (Spencer’s Retail Limited), among others.

Key strategies driving the market include investing in hyperlocal fulfilment, partnering with retail tech, enabling supplier digitisation, and leveraging ONDC connectivity.

High fragmentation, infrastructure gaps, vendor reliability, and demand unpredictability affect inventory flow and pricing stability.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Product |

|

| Breakup by Sector |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.