THE ACTIVATION ECONOMY: What NFHS-6 Reveals About India's Next Decade of Growth

India’s National Family Health Survey, NFHS-6, is one of the most consequential public datasets released in recent years. The May 2026 fact sheets, covering approximately 6.79 lakh households across 715 districts, offer far more than a health update. They provide a national-scale map of how India’s consumers, patients, households, and care systems are changing across health access, financial protection, digital behaviour, nutrition, and demographics. For government planners and development organizations, NFHS-6 is the evidence base for the next programme cycle. For private sector leaders and investors, it is a demand intelligence asset of the highest strategic Value.

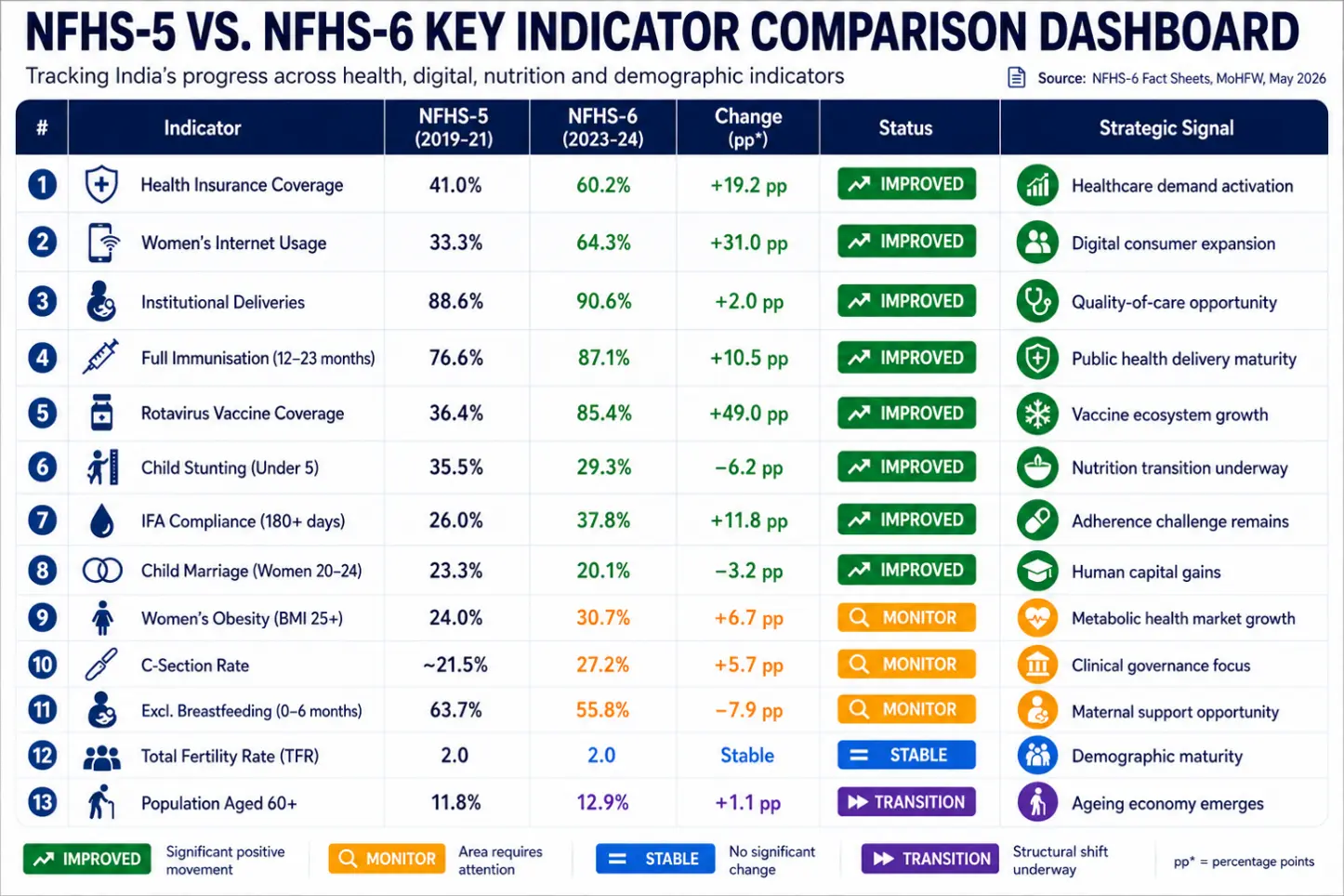

Its real value lies in what it reveals about India’s demand infrastructure, where households can be reached, which services they now access, which behaviours are changing, and where the gaps between policy intent and lived reality persist. Over the last decade, India has built substantial access infrastructure. Institutional deliveries stand at 90.6%, immunization has reached 87.1%, health insurance covers 60.2% of households, and women’s internet access has nearly doubled to 64.3%. The next decade will not be about building more access. It will be about activation, converting this infrastructure into consistent use, quality outcomes, and sustained social and commercial value.

NFHS-6 is not just a public health survey. It is the clearest national map of India’s transition from access to activation. For leadership teams across government, business, and development, the strategic question is the same: India has built the platform. What will it take to make it work better?

“India’s next decade will not be shaped only by who gets access. It will be shaped by whether access becomes use, trust, continuity, and measurable improvement.”

NFHS-5 vs. NFHS-6: Key Indicator Comparison

Source: NFHS-6 Fact Sheets, MoHFW (released May 2026).

Five Infrastructure Layers Now in Place

Viewed together, NFHS-6 suggests that India has built five foundational layers of infrastructure that will shape the country's next phase of growth. First, health access, with institutional deliveries reaching 90.6% and full immunization rising to 87.1%, demonstrates the ability to deliver services at population scale. Second, financial protection, with health insurance coverage increasing to 60.2%, is reducing financial barriers to care. Third, digital reach, with women's internet usage at 64.3%, is creating a powerful distribution channel for health, financial, and consumer services.

At the same time, two longer-term transitions are reshaping future demand. Demographic transition, reflected in a stable TFR of 2.0 and a growing 60+ population, is increasing the importance of chronic care and aging-related services. Nutrition transition, characterised by declining child stunting alongside rising adult obesity, highlights the emergence of a dual burden that requires different interventions, products, and policy responses.

These are not isolated indicators. Together, they form the foundations of India's Activation Economy, where the challenge is no longer expanding access, but turning existing infrastructure into greater utilization, better outcomes, and sustained impact.

SIGNAL 01: Health Insurance Crosses 60% - Activation, Not Enrolment, Is the Prize

Health insurance coverage has risen from 41.0% to 60.2%, driven by Ayushman Bharat PM-JAY, state-sponsored schemes, and growing private insurance penetration. For hospitals, insurers, TPAs, and diagnostic networks, this marks a fundamental shift in the healthcare landscape. The key question is no longer how many people are covered, but how effectively that coverage translates into healthcare utilization. As newly insured households begin seeking care that was previously deferred, particularly in Tier 2 and Tier 3 markets, organizations that understand utilization patterns by geography, channel, and patient segment will be best positioned to capture growth.

The implications extend well beyond healthcare providers. Hospitals need insurance-ready operating models, insurers must strengthen benefit awareness and renewal confidence, and digital health platforms have an opportunity to simplify claims and patient navigation. At the same time, a significant activation challenge remains. Nearly 40% of households are still uninsured, while many first-generation beneficiaries do not fully understand or utilise their entitlements. For government and development stakeholders, this underscores the importance of last-mile outreach, health literacy, and patient support mechanisms. Ultimately, the most sustainable value will be created by organizations that can convert coverage into utilization, engagement, and measurable health outcomes.

“Coverage expands the addressable market. Activation determines whether it converts into health outcomes, claims, and sustained engagement. The gap between the two is where policy and commercial strategy must now focus.”

| Signal Type |

Key Insight |

|

MARKET SIGNAL

|

- India Health Insurance Market

- India Health Insurance Market Size (FY2025): ~USD 15 billion

- Projected (2030): ~USD 46 billion at ~21% CAGR

- Key shift: Enrolment → utilization, retention, and claims intelligence

|

POLICY &

PROGRAMME |

- Ayushman Bharat Programme Dimensions

- PM-JAY coverage: 36.9 crore+ cards; 40M+ hospital admissions; 39.8% households still uncovered

- Last-mile activation: AB Health & Wellness Centres as first-contact care and entitlement awareness touchpoints

- SDG linkage: SDG 3.8 - Universal Health Coverage financial risk protection

|

SIGNAL 02: Immunization at 87.1% - A Proven System Capability, Not Just a Milestone

Full immunization among children aged 12 to 23 months has increased to 87.1%, while rotavirus vaccine coverage has more than doubled from 36.4% to 85.4%. The public health system remains the backbone of this success, with 95.6% of childhood vaccinations delivered through public facilities. Beyond the health gains, these figures demonstrate India's growing ability to execute large-scale public health programs through a combination of frontline outreach, digital beneficiary tracking, cold-chain management, and targeted interventions.

The significance extends far beyond immunization. The same capabilities that drive vaccination coverage, trusted frontline workers, household engagement, data tracking, and local execution are also critical for maternal health follow-up, nutrition programs, NCD screening, adult vaccination, and preventive care initiatives. For life sciences companies, this reinforces India's position as a sophisticated healthcare delivery environment rather than simply a high-volume market. For development organizations and programme managers, it provides a proven operational model for the next generation of health and behaviour change interventions. Immunization success is not just a public health achievement; it is a foundation for India's broader health activation agenda.

| Signal Type |

Key Insight |

|

MARKET

SIGNAL

|

- India Vaccines & Cold-Chain Market

- India Vaccine Market (2025): ~USD 3 billion, ~12% CAGR

- Next commercial opportunity: HPV, adult immunization, next-generation antigens, biologic introductions

- Cold-chain market: USD 500M+, growing at ~15% CAGR as public system expands

- Data infrastructure: U-WIN digital vaccination records - new engagement layer for child health platforms

|

POLICY &

PROGRAMME |

- Universal Immunization Programme Dimensions

- Public delivery dominance: 95.6% of vaccinations through government facilities - private role supplementary

- Template value: UIP delivery model ( ASHA outreach, cold-chain, U-WIN tracking) replicable for NCD and preventive care

- SDG linkage: SDG 3.b - vaccine access; SDG 3.2 - under-5 mortality reduction

|

SIGNAL 03: Maternal care has entered the quality and continuity phase

NFHS-6 confirms continued progress in maternal and child healthcare. Antenatal care registration has increased to 95.9%, institutional deliveries to 90.6%, and skilled birth attendance to 91.3%, reflecting the impact of programs such as JSY, JSSK, SUMAN, and PMSMA. These gains show that India has built a strong maternal health access platform.

The challenge now is continuity and quality of care. While almost all women register for antenatal care, only 65.2% complete four or more ANC visits, highlighting a significant drop-off across the care journey. At the same time, exclusive breastfeeding has declined from 63.7% to 55.8%, signalling the need for stronger postnatal support and counselling. For healthcare providers, the opportunity is no longer limited to the delivery event itself but extends across the full maternal and child health continuum, including antenatal diagnostics, risk monitoring, maternal nutrition, lactation support, postnatal care, and early childhood health. Rising C-section rates, now at 27.2%, further reinforce the importance of quality, clinical governance, and appropriate care pathways. The next phase of India's maternal health agenda will be defined not by access, but by continuity, outcomes, and patient experience.

| Signal Type |

Key Insight |

|

MARKET

SIGNAL

|

- India Maternal Health & Obstetric Care Market

- India Maternal Health Market Size (2025): ~USD 3.5 billion, ~10% CAGR

- Commercial opportunity: Postnatal care, neonatal ICU, obstetric MedTech, maternal nutrition

- Governance risk: C-section at 27.2% national / ~40% urban - utilization review and clinical audit increasingly important

|

|

POLICY &

PROGRAMME

|

- Maternal Health Programme Dimensions

- Programme drivers: JSY, JSSK, PMSMA, SUMAN, PMMVY 2.0 - delivery and ANC coverage largely achieved

- Critical gap: Breastfeeding decline (63.7%→55.8%) and incomplete ANC cascade require MAA reinforcement and ASHA follow-up

- SDG linkage: SDG 3.1 (maternal mortality) and 3.2 (neonatal mortality) - quality now the binding constraint, not access

|

SIGNAL 04: Women’s Digital Reach at 64.3% - From Digital Inclusion to Economic Participation

Women’s digital and financial inclusion is emerging as one of the most important shifts highlighted by NFHS-6. Women’s internet usage has nearly doubled from 33.3% to 64.3%, while bank account ownership has increased to 89.0% and personal mobile phone usage to 63.6%. Together, these indicators suggest that India’s digital and financial infrastructure has reached a scale where it can serve as a powerful channel for healthcare, financial services, consumer engagement, and public programme delivery.

The implications extend well beyond connectivity. A digitally connected woman is often a key healthcare decision-maker, caregiver, household influencer, and financial participant. For healthcare organizations, this creates opportunities for mobile-first maternal health services, reproductive health education, appointment reminders, chronic disease counselling, and postnatal follow-up. For insurers, financial institutions, and consumer brands, it enables more direct engagement, education, and service delivery at scale. At the same time, platforms such as the Ayushman Bharat Digital Mission and the growing adoption of ABHA IDs are creating the digital foundations for more personalized, longitudinal health interventions. The strategic shift is clear: women should no longer be viewed simply as beneficiaries, but as primary users, decision-makers, and distribution anchors within India's evolving activation economy.

| Signal Type |

Key Insight |

|

MARKET

SIGNAL

|

- India Digital Health & Consumer Technology Market

- India Digital Health Market (2025): ~USD 6.5 billion, ~28% CAGR

- Women-first digital services: Fastest-growing sub-segment: telemedicine, FMCG D2C, maternal platforms

- Commercial imperative: Vernacular, mobile-first, women-centred channel design across all consumer sectors

|

|

POLICY &

PROGRAMME

|

- Digital Inclusion Programme Dimensions

- ABDM: National digital health identity infrastructure enabling targeted, longitudinal programme delivery

- Community networks: Self-Help Groups as digital literacy multipliers and SBCC amplifiers at community level

- SDG linkage: SDG 5.b (technology for women’s empowerment) and SDG 3 (digital health communication)

|

SIGNAL 05: Child Stunting Falls to 29.3% While Women's Obesity Reaches 30.7% – India's Nutrition Market Has Split in Two

NFHS-6 shows encouraging progress in child nutrition, with stunting declining from 35.5% to 29.3%, severe wasting falling from 7.7% to 5.2%, and improvements in infant feeding practices. These gains reflect sustained investments through POSHAN Abhiyaan, POSHAN 2.0, ICDS, maternal nutrition programs, and frontline counselling. Yet the challenge remains substantial, with nearly one in three children still stunted and diet diversity continuing to lag.

At the same time, women's obesity has increased from 24.0% to 30.7%, highlighting the growing burden of overweight, metabolic risk, and lifestyle-related diseases. Together, these trends show that India is now managing two nutrition realities at once: persistent undernutrition alongside rising obesity.

For businesses and policymakers, this means a single nutrition strategy is no longer enough. One track must focus on maternal and child nutrition, micronutrients, and vulnerable populations, while the other addresses preventive nutrition, healthy diets, weight management, and NCD prevention. For FMCG, nutrition, healthcare, and pharmaceutical companies, these represent two distinct growth markets requiring different products, channels, and engagement strategies.

“India’s nutrition market has split-one track for the first 1,000 days, one for rising metabolic risk. Any strategy built for only one of these realities addresses less than half the challenge.”

| Signal Type |

Key Insight |

|

MARKET

SIGNAL

|

- India Nutraceuticals & Clinical Nutrition Market

- India Plant-Based Nutraceuticals Market Size (2026): ~USD 8 billion, ~18% CAGR

- Fastest-growing sub-segment: Metabolic health: ~24% CAGR (diabetes, weight management, preventive nutrition)

- Therapeutic / first-1000-days: Fortified foods, therapeutic nutrition, micronutrient supplementation

- Key gap: Only 15.1% of 6-23 month children receive adequate diet - complementary feeding opportunity

|

|

POLICY &

PROGRAMME

|

- POSHAN & Nutrition Programme Dimensions

- POSHAN 2.0 / Saksham Anganwadi: Convergent programme: supplementary nutrition, counselling, growth monitoring for mothers and children

- Critical unfinished agenda: Complementary feeding gap (15.1% adequate diet) requires SBCC investment alongside product supply

- SDG linkage: SDG 2.2 (end all forms of malnutrition by 2030) - dual-burden requires dual programme approach

|

SIGNAL 06: IFA Compliance Reaches 37.8% - Why Coverage Alone Is Not Enough

Maternal nutrition indicators have improved, with the proportion of pregnant women consuming iron and folic acid (IFA) supplements for 100 or more days increasing from 44.1% to 54.9%, and completion of the full 180-day course rising from 26.0% to 37.8%. While this represents meaningful progress, nearly two-thirds of pregnant women still do not complete the recommended course.

This highlights one of NFHS-6's most important lessons: expanding programme coverage does not automatically translate into better outcomes. Many women receive supplements but do not complete the full course due to side effects, low awareness, household constraints, or inadequate follow-up. The challenge is no longer product availability, but sustained adherence.

For healthcare, nutrition, and pharmaceutical organizations, this creates opportunities to improve counselling, patient support, formulation design, reminder systems, and targeted screening. For government and development programs such as Anaemia Mukt Bharat, the priority is to strengthen last-mile engagement and behaviour change. The message from NFHS-6 is clear: the greatest gains will come not from distributing more products, but from helping people use them consistently and effectively.

| Signal Type |

Key Insight |

|

MARKET

SIGNAL

|

- India Iron & Nutritional Supplements Market

- India Iron Supplements Market (2025): ~USD 1.2 billion, ~11% CAGR

- Commercial frontier: Adherence: reformulation, palatable formats, digital monitoring, counselling integration

- Diagnostic adjacency: Point-of-care anaemia screening to tailor supplementation by type and severity

|

|

POLICY &

PROGRAMME

|

- Anaemia Mukt Bharat Programme Dimensions

- AMB strategy: 3-pronged: IFA supplementation + deworming + dietary diversification across six beneficiary groups

- Binding constraint: Supply largely solved; adherence, counselling quality, and follow-up are the remaining gaps

- Programme implication: ASHA-led household counselling on side-effect management is highest-leverage available intervention

|

SIGNAL 07: Total Fertility Rate Remains at 2.0 – A New Demand Landscape Is Emerging

India's total fertility rate (TFR) remains stable at 2.0, while contraceptive prevalence has increased from 66.7% to 69.1%. This confirms that India has largely completed its demographic transition at the national level, although important differences remain across states.

For business and policy leaders, fertility is more than a demographic indicator. It is a long-term demand signal that shapes future needs in maternal and child health, education, housing, healthcare, and financial services. As fertility stabilises, growth in some child-focused categories may moderate, while demand for adult healthcare, chronic disease management, elder care, and long-term financial protection is likely to increase.

The implications will vary by geography. Some states will continue to see strong demand for reproductive and child health services, while others will move more rapidly towards aging-related healthcare and social support needs. NFHS-6 highlights the importance of looking beyond national averages and planning for India's increasingly diverse demographic realities.

| Category |

Programme Details |

|

MARKET

SIZING

SIGNAL

|

- India Reproductive Health & Family Planning Market

- India Contraceptives Market (2025): ~USD 800 million, growing at ~9% CAGR

- Paediatric-to-adult shift: Adult NCD, geriatric, and chronic categories will outpace paediatric volume growth

- Geographic dimension: State-level TFR variation demands localised strategy: not one national market but 28+ sub-markets

|

SIGNAL 08: Population 60+ Reaches 12.9% - Aging Is a Core Market and Programme Variable

The share of India's population aged 60 and above has increased from 11.8% to 12.9%, highlighting a gradual but important demographic shift. As India's population ages, healthcare needs are becoming more complex, with growing demand for chronic disease management, diagnostics, long-term medication, rehabilitation, home care, and caregiver support.

For healthcare providers, pharmaceutical companies, diagnostics firms, insurers, and eldercare providers, this represents a long-term structural growth opportunity. Demand is likely to increase for senior-focused healthcare services, preventive screening, home-based care models, and financial protection products tailored to older adults. At the same time, public systems are beginning to respond through initiatives such as expanded PM-JAY coverage for senior citizens, geriatric care programs, and screening services at Health and Wellness Centres.

NFHS-6 reinforces that aging is no longer a future challenge. It is a present reality that will increasingly shape healthcare demand, service delivery, and policy priorities over the coming decade.

“India’s aging population is not a future policy challenge. With 185 million older adults today and 340 million projected by 2050, it is a present and rapidly growing commercial and social reality.”

| Signal Type |

Key Insight |

|

MARKET

SIGNAL

|

- India Senior Care & Chronic Disease Management Market

- India Elderly Care Products Market (2025): ~USD 8.5 billion, ~20% CAGR

- Projected Market (2030): ~USD 20 billion

- Population 60+: ~185M today; ~230M by 2031; ~340M by 2050

- Key demand categories: NCD management, home care, geriatric diagnostics, senior insurance, rehabilitation

|

|

POLICY &

PROGRAMME

|

- Aging Population Programme Dimensions

- NPHCE: Geriatric wards in district hospitals, primary care outreach for elderly-infrastructure thin relative to need

- Infrastructure gap: Geriatric specialists, palliative care, dementia management, and caregiver support remain severely under-resourced

- SDG linkage: SDG 3.4 (reduce premature NCD mortality by one-third by 2030)

|

SIGNAL 09: Child Marriage Falls to 20.1% - Progress Is Real, but the Challenge Remains

The proportion of women aged 20 to 24 married before 18 has declined from 23.3% to 20.1%, reflecting progress in girls' education, social protection programs, and awareness efforts. However, child marriage remains a significant challenge, particularly in several high-burden states.

Beyond being a social issue, child marriage is closely linked to adolescent pregnancy, poorer maternal and child health outcomes, lower educational attainment, and reduced economic opportunity. For governments, development organizations, and CSR programs, the findings highlight the need to address the underlying economic and social drivers of early marriage. Reducing child marriage is ultimately an investment in healthier, more educated, and economically empowered future generations.

| Category |

Programme Details |

|

POLICY &

PROGRAMME

|

- Child Marriage Prevention Programme Dimensions

- State variation: Bihar: 34.6% vs. national 20.1% - national average masks deep geographic inequity requiring state-specific strategies

- Programme redesign needed: Economic incentives + girls’ education + RKSK adolescent health + POCSO enforcement must converge

- SDG linkage: SDG 5.3 (end child marriage by 2030) - India is off-track on current trajectory

|

SIGNAL 10: The Activation Era Has Begun - Infrastructure Now Demands Outcomes

The most important signal from NFHS-6 is not a single indicator, but the pattern across them all. India has built much of the infrastructure required for broad-based access: institutional deliveries have reached 90.6%, immunization coverage is rising, health insurance now covers 60.2% of households, and women's digital access has expanded rapidly. Yet many indicators reveal a persistent gap between access and outcomes. Only 65.2% of women complete four or more ANC visits despite 95.9% registering, full IFA compliance remains at 37.8%, and just 15.1% of young children receive an adequate diet.

This reflects a fundamental shift in India's development journey. The challenge is no longer simply expanding access, but ensuring that people consistently use and benefit from the services available to them. For governments and development organizations, this means designing programs around utilization, adherence, and behaviour change. For businesses, it creates opportunities for products, services, and platforms that improve engagement, continuity of care, and outcomes. NFHS-6 suggests that India's next phase of progress will be defined not by building more infrastructure, but by making existing infrastructure work better.

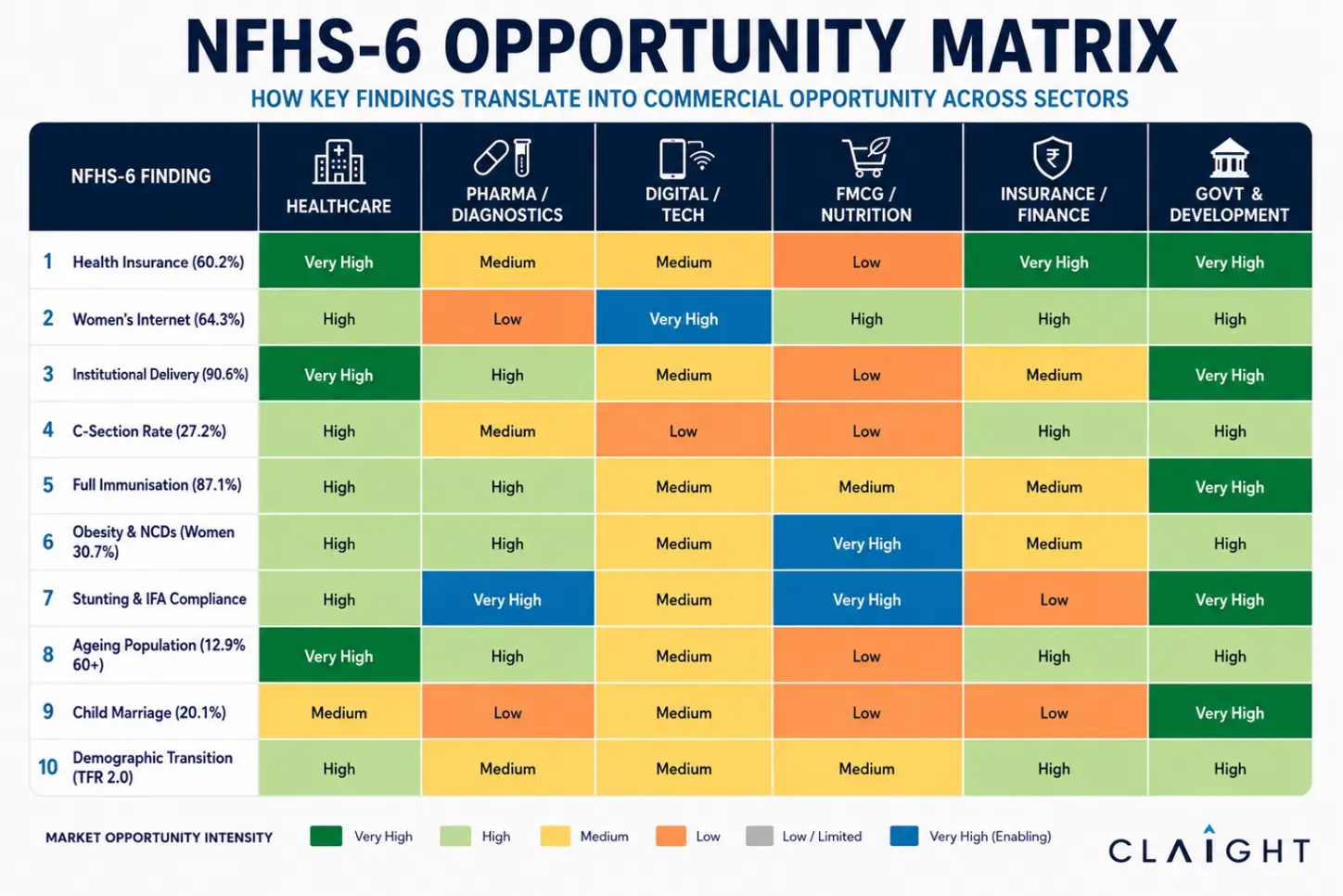

The Opportunity Matrix: NFHS-6 Signals Across All Sectors

The heat-map below structures NFHS-6’s ten findings against key stakeholder sectors.

| NFHS-6 FINDINGS × SECTORS OPPORTUNITY HEAT-MAP |

| NFHS-6 Finding |

Healthcare |

Pharma & Dx |

Digital / Tech |

FMCG / Nutrition |

Insurance & Finance |

Govt & Development |

| Health Insurance (60.2%) |

Very High |

Medium |

Medium |

Low |

Very High |

Very High |

| Women's Internet (64.3%) |

High |

Low |

Very High |

High |

High |

High |

| Institutional Deliveries (90.6%) |

Very High |

High |

Medium |

Low |

Medium |

Very High |

| C-Section Rate (27.2%) |

High |

Medium |

Low |

Low |

High |

High |

| Full Immunization (87.1%) |

High |

High |

Medium |

Low |

Medium |

Very High |

| Obesity & NCDs (Women 30.7%) |

High |

High |

Medium |

Very High |

Medium |

High |

| Stunting & IFA Compliance |

High |

Very High |

Medium |

Very High |

Low |

Very High |

| Aging Population (12.9% 60+) |

Very High |

High |

Medium |

Low |

High |

High |

| Child Marriage (20.1%) |

Medium |

Low |

Medium |

Low |

Low |

Very High |

| Demographic Transition (TFR 2.0) |

High |

Medium |

Medium |

Medium |

High |

High |

Legend: Navy = Very High | Teal = High | Amber = Medium | Grey = Low | Green column = Government & Development sector priority

Five Strategic Imperatives

The ten signals from NFHS-6 point to five cross-sector imperatives that are relevant to governments, development organizations, investors, and private sector leaders alike.

| No. |

Imperative |

Guidance |

| 01 |

Reorient from Access to Activation |

Infrastructure is substantially in place. Value-whether measured in health outcomes or commercial returns-now lies in utilization, adherence, and quality. Design for completion of the care cascade, not just coverage. |

| 02 |

Invest in State and District Granularity |

NFHS-6 highlights significant state and district-level variation across indicators. Effective programme design, investment decisions, and go-to-market strategies require a more localised understanding of demand and need. |

| 03 |

Treat Women's Digital Reach as Core Infrastructure |

With 64.3% of women now using the internet, digital engagement is no longer a niche channel. Mobile-first, vernacular, and women-centred approaches should be embedded in health, financial, and consumer service strategies. |

| 04 |

Adopt a Dual-Track Nutrition Strategy |

Stunting and obesity coexist. Child therapeutic nutrition and adult metabolic health require distinct product architectures, programme designs, and channel strategies. A single approach addresses only half the market and half the problem. |

| 05 |

Embed Demographics Into Long-Range Plans |

Fertility has stabilised at 2.0 while the population aged 60+ continues to grow. Long-term planning should account for increasing demand for chronic care, elder services, financial protection, and age-related support systems. |

“India has built the infrastructure of access. The next decade belongs to those who can activate it-converting coverage into outcomes, enrolment into engagement, and investment into sustained value. This is the shared challenge for government, development, and private sector alike.”

How Claight Can Help

Claight Corporation translates complex public datasets into actionable intelligence for organizations across India’s healthcare, consumer, and development markets. Our work spans market assessments, opportunity sizing, state and district prioritisation, consumer and patient segmentation, stakeholder mapping, programme design support, and strategy formulation. We serve private sector clients-healthcare providers, pharma, insurers, FMCG brands, investors-as well as government agencies, multilateral organizations, NGOs, and development finance institutions. To translate NFHS-6 into actionable strategy, schedule a briefing with our research team at claight.com.

Share