Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

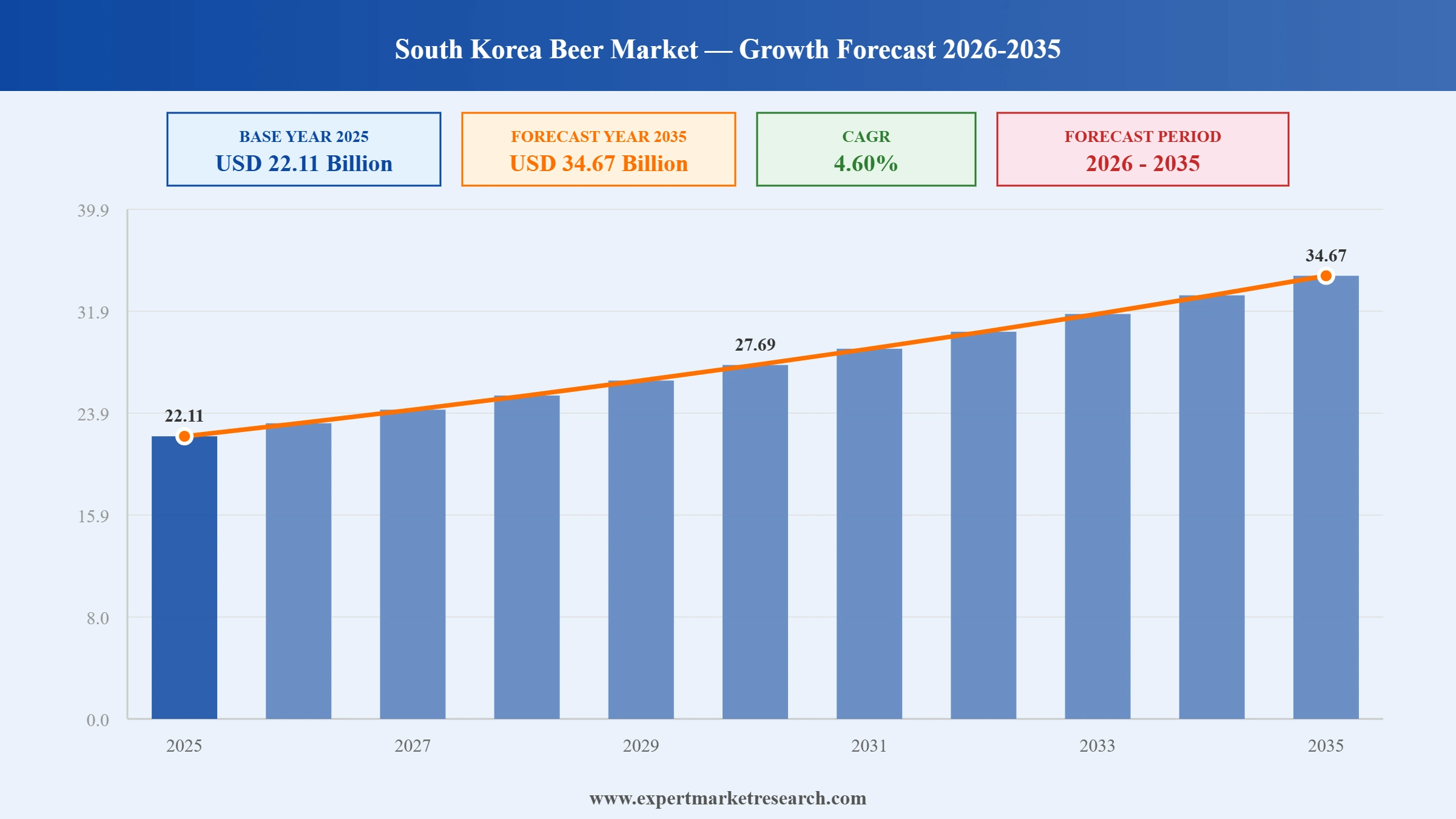

The South Korea beer market reached a value of USD 22.11 Billion at 2025 and is projected to expand at a CAGR of around 4.60% during the forecast period of 2026-2035. With rising consumer preference for premium and craft beer varieties, growing penetration of convenience retail channels, increasing availability of international beer brands, and the robust expansion of the on-trade dining segment, the market is expected to reach USD 34.67 Billion by 2035.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South Korea's beer market is going through meaningful structural shifts, with premiumisation, craft beer adoption, and convenience retail expansion reshaping how consumers engage with the category. Multinational brewers are deepening their local footprint while domestic brands respond with product innovation and new packaging formats. These converging dynamics are creating a more diverse, competitive, and opportunity-rich market for all participants.

Oriental Brewery expanded its craft beer portfolio in May 2025, introducing a range of small-batch ales aimed at South Korea's growing millennial and Gen Z consumer base. The launch targeted the on-trade channel, placing products across premium bars and gastropubs in Seoul and Busan, signalling a deliberate push into the fast-growing premium beer segment.

Hite Brewery Company Limited unveiled a low-calorie extension of its flagship Terra beer brand in February 2025, responding to heightened consumer demand for health-conscious beverage options. The new variant was rolled out nationally through both convenience stores and hypermarkets, broadening the brand's appeal and reinforcing its competitiveness in the evolving South Korea beer space.

Heineken N.V. announced a strengthened distribution partnership with a leading South Korean beverage distributor in October 2024, aiming to expand its retail presence across convenience stores and specialised shops. The move reflects Heineken's deliberate strategy to capture a larger share of South Korea's growing premium and imported beer segment through a more robust ground-level distribution network.

Lotte Chilsung Beverage Co., Ltd. acquired a minority stake in a South Korean craft beer start-up in July 2024, marking a strategic move to diversify its beer portfolio beyond mainstream lager. The investment supports Lotte Chilsung's broader ambition to compete effectively in the fast-growing craft and premium beer categories through financial backing and distribution scale.

The South Korea beer market is seeing accelerating craft beer adoption, particularly in metropolitan centres like Seoul, Busan, and Incheon. Breweries such as Magpie Brewing Co. and Galmegi Brewing Co. have expanded their tap-room networks and retail partnerships throughout 2024, reinforcing craft beer's position as a mainstream consumer preference rather than a niche offering.

South Korea beer market growth is increasingly being driven by convenience store chains, which have expanded dedicated beer sections and chilled display units across their networks. GS25 and CU, two of South Korea's largest convenience store operators, reported growing beer category revenues in 2024, driven by demand for imported, craft, and premium domestic brands across urban and suburban outlets.

Despite gradual can packaging growth, glass bottles remain the format of choice in South Korea's restaurants and bars, where premiumisation drives buyer decisions and presentation matters. Leading brewers including Hite Brewery and Oriental Brewery have continued investing in glass bottling infrastructure as part of their South Korea beer market on-trade strategy throughout 2024.

International beer brands are gaining shelf space across South Korean hypermarkets and specialised shops. Heineken, Asahi, and several European craft labels have expanded their SKU counts in major retail chains through late 2024, reflecting a clear consumer appetite for variety and the broader premiumisation trend running through the South Korea beer industry's retail distribution landscape.

A growing segment of South Korean consumers is exploring low-alcohol and non-alcoholic beer options, prompting mainstream brewers to respond with product line expansions. Oriental Brewery and Hite Brewery both introduced or extended their reduced-alcohol offerings in the South Korea beer market during 2024, tapping into health-conscious consumer segments that continue to grow across urban demographics.

The report of Expert Market Research's titled "South Korea Beer Market Report and Forecast 2026-2035" offers a detailed analysis of the market based on the following segments:

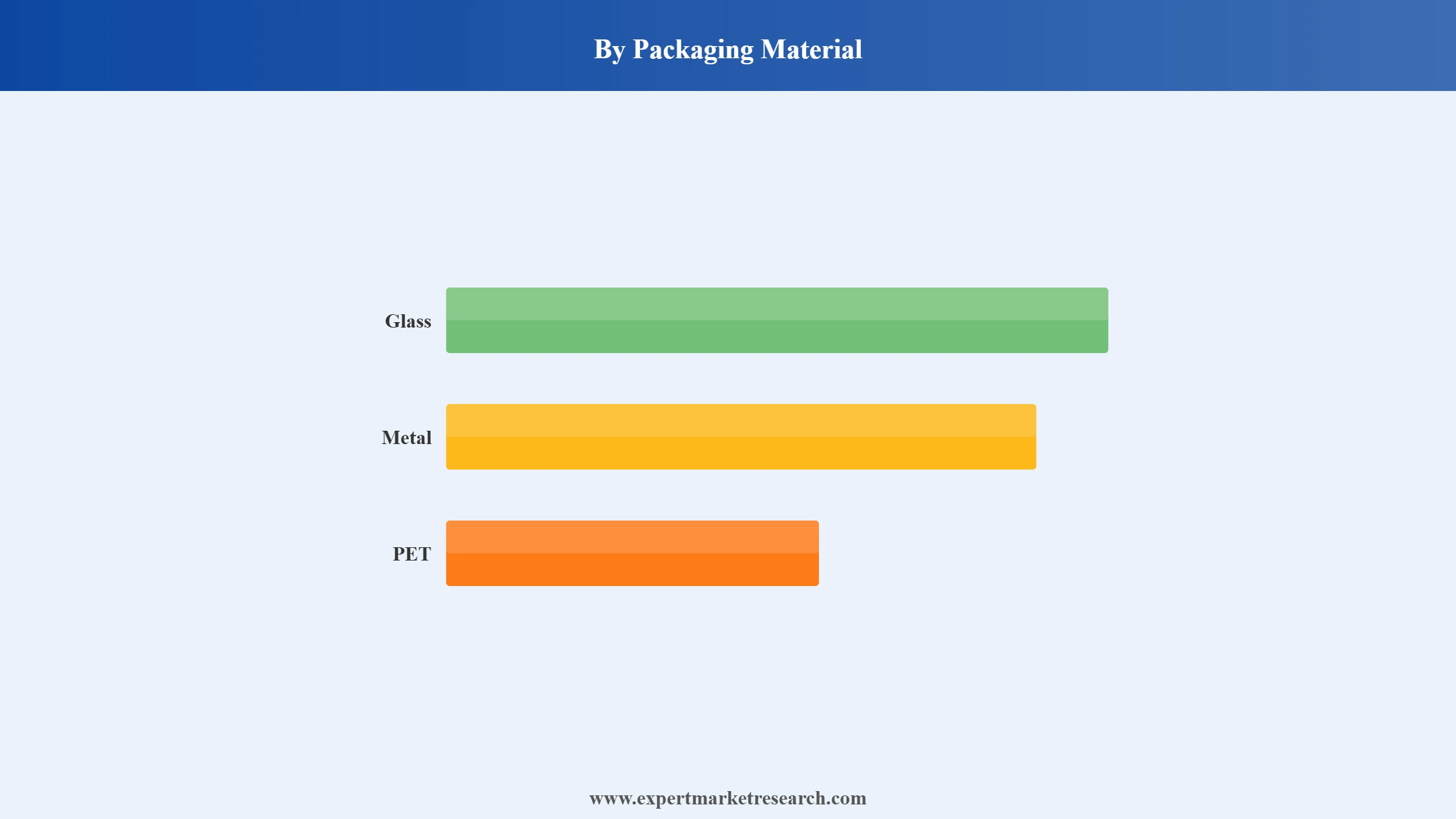

Market Breakup by Packaging Material

Key Insight: Glass packaging holds the dominant position in South Korea's beer packaging market, largely due to its premium consumer perception and widespread use in bars, restaurants, and premium retail. Metal cans have been gaining traction, particularly for convenience store retail and ready-to-drink consumption occasions. The PET segment, while smaller, maintains relevance in economy-tier offerings. South Korea's shift toward premiumisation continues to reinforce glass as the default format for both domestic and imported beer brands targeting on-trade and upper-retail channels.

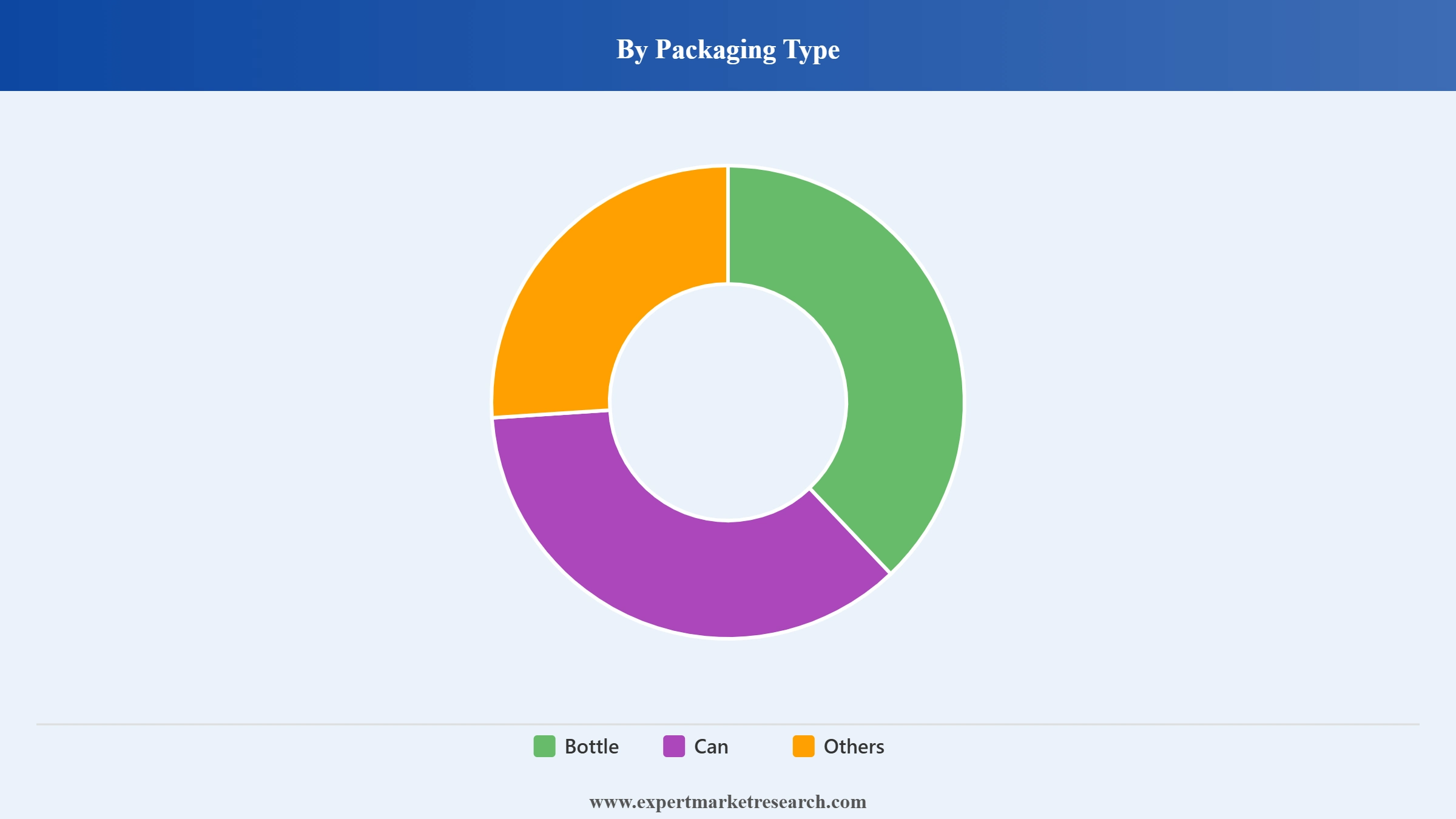

Market Breakup by Packaging Type

Key Insight: Bottles remain the leading packaging type in the South Korea beer market, driven by their strong association with premium dining occasions and well-established consumer habits in restaurants and entertainment venues. Cans have seen growing adoption, particularly through convenience stores and home consumption settings where portability and chilled storage convenience are key purchase factors. The others segment includes draught formats used primarily in the on-trade channel. The gradual shift toward convenience-oriented consumption is elevating the can segment's share, though bottles continue to lead on value terms.

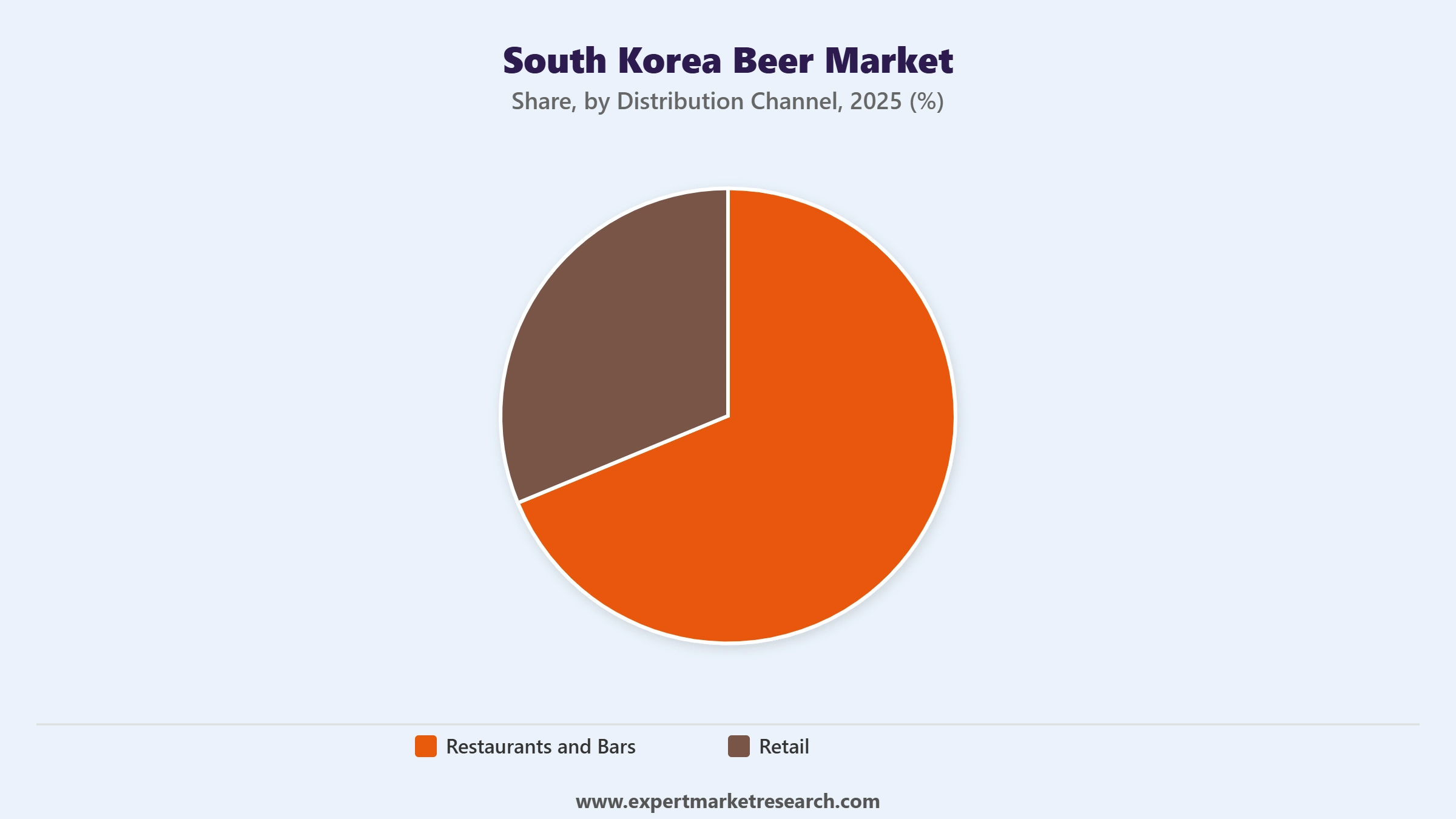

Market Breakup by Distribution Channel

Key Insight: Restaurants and bars represent a critical distribution pillar for the South Korea beer market, anchored in the country's deeply rooted social drinking culture in hofs, chimaek establishments, and Korean barbecue venues. However, retail channels, particularly convenience stores, have been gaining meaningful ground. South Korea's roughly 50,000 convenience store outlets, dominated by GS25, CU, and 7-Eleven Korea, serve as highly accessible and high-frequency beer purchase points. Hypermarkets cater to bulk purchase occasions, while specialised shops support craft and premium beer segments through curated assortments.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By Packaging Material, glass dominates the market due to premium positioning and strong on-trade channel preference

Glass packaging accounts for the largest share of the South Korea beer market, supported by its long-standing dominance in the on-trade channel where visual presentation drives purchasing behaviour. Bars, restaurants, and entertainment venues overwhelmingly prefer glass bottles for serving beer, and major domestic brewers including Hite Brewery Company Limited and Oriental Brewery have consistently maintained investment in glass bottling infrastructure. The perceived quality advantage of glass over cans or PET containers further cements its leading position among premium beer consumers in South Korea's urban markets.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

While glass leads, metal cans are making meaningful inroads across retail channels, particularly among younger consumers who value portability and convenience. The growing popularity of home consumption occasions has accelerated can adoption, with Oriental Brewery's Cass and Hite Brewery's Terra brands widely available in can formats across South Korean convenience stores. Metal packaging is expected to register a healthy growth trajectory over the forecast period, supported by expanding product lines and promotional activities in the retail channel.

By Packaging Type, bottles account for the dominant share of the market due to their premium appeal and established on-trade penetration

Bottles represent the preferred packaging format in South Korea's beer market, aligned with premium consumption occasions and well-established consumer habits in dining and entertainment settings. Both domestic beers and imported brands predominantly enter the on-trade channel in glass bottle format, where price-per-unit tends to be higher, driving stronger value contribution. South Korea's restaurant and bar ecosystem, a core beer consumption venue for decades, sustains reliable demand for bottled beer across urban and suburban markets alike.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Cans represent the fastest-growing packaging type segment, especially in convenience store and home consumption contexts. Product launches in can format have increased considerably, with brands extending their range into new flavours and seasonal limited editions. In 2024, several domestic brewers and importers expanded their can SKU portfolios in direct response to growing demand from South Korea's convenience store operators, which reported strengthened volumes in the chilled beer category throughout the year.

By Distribution Channel, restaurants and bars account for the dominant share of the market due to South Korea's strong on-trade drinking culture

The on-trade channel, encompassing restaurants and bars, has historically led South Korea's beer distribution landscape, anchored in the country's distinctive dining and socialising culture. Beer is a staple accompaniment in hofs, chimaek restaurants, and Korean barbecue establishments, creating sustained baseline demand across cities and regional towns. Major brewers including Hite Brewery Company Limited and Oriental Brewery have maintained dedicated on-trade sales teams and logistics networks to serve this channel with competitive speed and reliability.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Retail channels are rapidly gaining strategic importance in South Korea's beer distribution mix. Convenience stores in particular have become a primary beer destination, with GS25 and CU actively curating imported and premium domestic beer assortments to meet evolving consumer preferences. The retail segment has been further energised by the growth of specialised beer shops offering curated craft and imported selections, which appeal to a more knowledgeable and experimentally minded consumer base seeking variety beyond mainstream lager brands.

South Korea's beer market is moderately concentrated, with two domestic brewers, Oriental Brewery and Hite Brewery Company Limited, commanding the majority of market volume. International players such as Heineken N.V. and LOTTE Asahi Co., Ltd. hold meaningful import-driven positions, particularly in the premium and convenience retail channels. The market has seen intensifying competition from the craft beer segment, where smaller, regionally focused brewers such as Magpie Brewing Co., Galmegi Brewing Co., and Jeju Beer Co., Ltd. are carving out loyal consumer followings through product differentiation and experience-led retail.

The competitive environment is increasingly shaped by premiumisation strategies, health-oriented product innovation, and aggressive expansion into convenience retail. Established players are investing in product line extensions and packaging innovations to defend market share while craft brewers focus on community engagement and tap-room network growth. The entry of conglomerate-backed entities such as Lotte Chilsung Beverage Co., Ltd. and BK Co., Ltd. further intensifies competition, bringing significant distribution scale and brand marketing resources into the beer category.

Founded in 1952 and headquartered in Seoul, South Korea, Oriental Brewery (OB) is a subsidiary of Anheuser-Busch InBev, the world's largest brewing company. OB holds a leading position in South Korea's beer market, with flagship brands including OB Golden Lager, Cass, and Hanmac. The company operates large-scale brewing facilities across South Korea and maintains a broad distribution network covering on-trade venues and all major retail formats. OB's global parent backing provides strong marketing investment and continuous product innovation capability.

Established in 1933 and headquartered in Seoul, Hite Brewery Company Limited is one of South Korea's oldest and most recognised brewing companies. Its flagship Terra brand, launched in 2019, has rapidly become one of the country's top-selling beers. Hite Brewery also operates in the spirits segment through its affiliate Hite Jinro. The company's extensive distribution infrastructure and strong brand equity across both on-trade and retail channels make it a formidable and deeply embedded competitor in South Korea's beer industry.

Founded in 1873 and headquartered in Amsterdam, Netherlands, Heineken N.V. is one of the world's largest and most internationally recognised brewing groups. In South Korea, Heineken operates through distribution partnerships and has established a solid presence in the premium import segment. Its flagship Heineken lager and portfolio brands such as Tiger are widely available across Korean retail and on-trade channels. Heineken leverages global marketing capabilities and strong brand recognition to target South Korean consumers seeking authentic international beer experiences.

Founded in 1950 and headquartered in Seoul, Lotte Chilsung Beverage Co., Ltd. is a subsidiary of the Lotte Group, one of South Korea's largest conglomerates. The company entered the beer market through its Kloud and FiLite brands, positioning them as premium domestic alternatives to imported lagers. Lotte Chilsung benefits from the Lotte Group's extensive retail network, including Lotte Mart hypermarkets, which provides a significant distribution advantage. The company continues to invest in product innovation to strengthen its foothold in South Korea's competitive beer category.

Other key players in the market are LOTTE Asahi Co., Ltd., BK Co., Ltd., Magpie Brewing Co., Galmegi Brewing Co., Jeju Beer Co., Ltd., and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Gain a clear competitive edge with our comprehensive South Korea beer market report for 2026. Packed with granular data on packaging preferences, distribution channel shifts, craft beer momentum, and leading player strategies, this report equips you with the intelligence needed to make confident decisions. Whether you are entering the South Korean beer sector for the first time or refining your existing market strategy, our insights offer precision and clarity. Download your free sample today and unlock the full potential of South Korea's dynamic beer landscape.

Argentina Beer Market

Australia Beer Market

India Beer Market

Craft Beer Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

At 2025, the market reached an approximate value of USD 22.11 Billion.

The market is projected to grow at a CAGR of 4.60% between 2026 and 2035.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach USD 34.67 Billion by 2035.

Key strategies driving the market include investing in smart packaging, partnering with themed venues, expanding regional SKUs, and leveraging sustainability for branding.

The implementation of a volume-based liquor tax on beer as well as premiumization are the key trends in the South Korean beer market.

The dominant types of beer packaging in the industry are bottle and cans.

The leading distribution channels in the market are into retail and restaurants and bars.

The key players in the market include Oriental Brewery, Hite Brewery Company Limited, Heineken N.V., Lotte Chilsung Beverage Co., LTD., LOTTE Asahi Co., Ltd., BK Co.,Ltd., Magpie Brewing Co., Galmegi Brewing Co., Jeju Beer Co., Ltd., and Others.

The key challenges are market saturation, intense price wars, and regulatory complexities around alcohol advertising are primary hurdles. Additionally, maintaining taste consistency in small batches poses quality control issues for craft brewers.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Packaging Material |

|

| Breakup by Packaging Type |

|

| Breakup by Distribution Channel |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.