Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

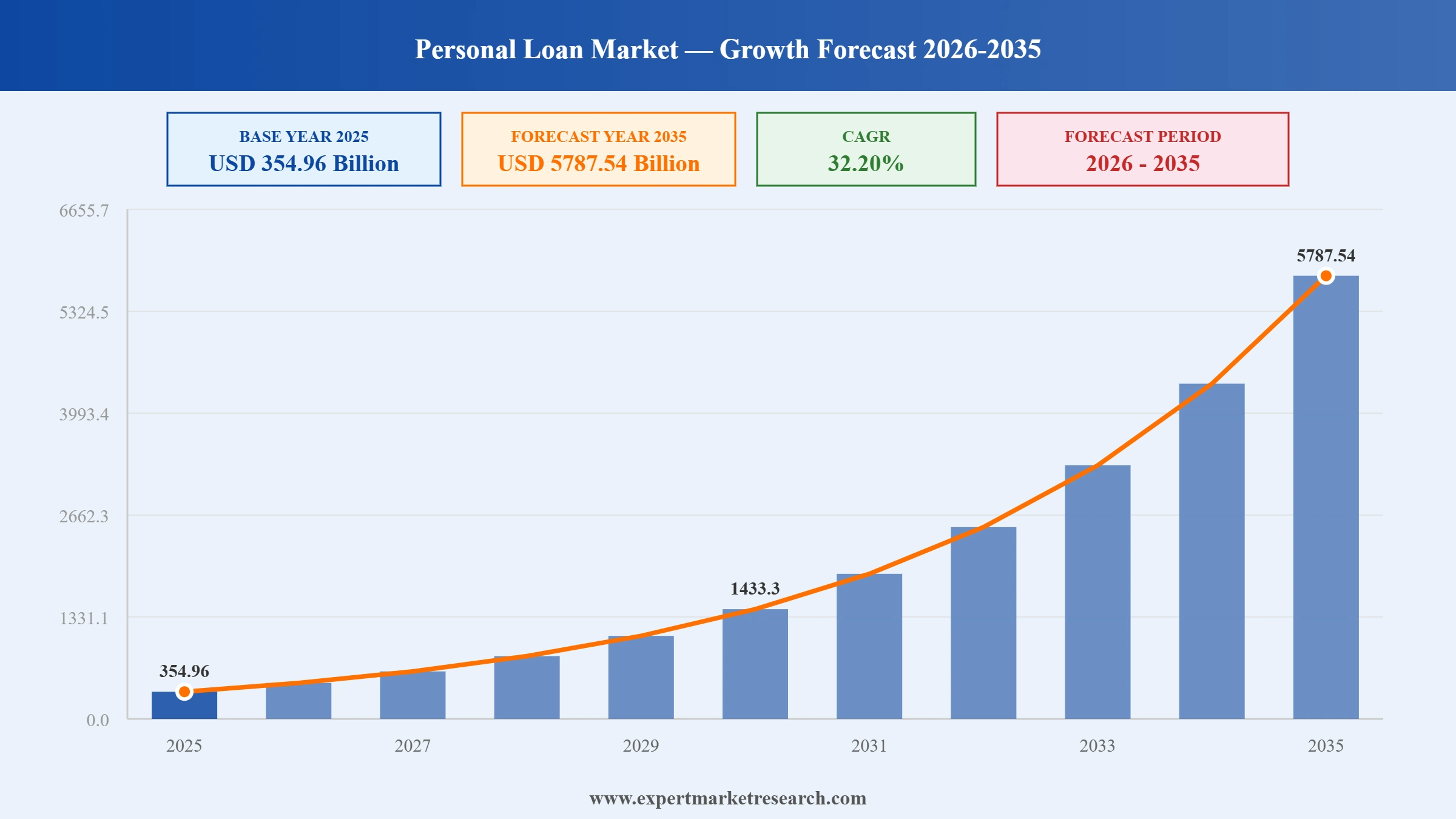

The global personal loan market reached a value of USD 354.96 Billion at 2025 and is projected to expand at a compound annual growth rate CAGR of around 32.20% during the forecast period of 2026-2035, reaching USD 5787.54 Billion by 2035. This remarkable growth trajectory is underpinned by accelerating digital lending adoption, the deepening integration of financial technology into everyday borrowing, the broadening of credit access across emerging economies, and rising consumer appetite for flexible short-term financing solutions.

Personal loans occupy a foundational position within the global consumer finance ecosystem. As unsecured credit instruments, they provide individuals with immediate access to capital without the encumbrance of asset pledging, making them one of the most versatile and widely deployed retail financial products globally. The market spans a broad spectrum of lender types, from conventional banking institutions and credit unions to digital-native fintech lenders and peer-to-peer platforms, each serving distinct borrower segments with differentiated products, underwriting standards, and distribution channels. The overall market landscape reflects a structural shift underway across the global lending industry. Traditional bank-dominated origination models are being supplemented, and in certain segments displaced, by technology-enabled platforms that deliver faster credit decisions, lower documentation burdens, and more personalized loan terms. Rising smartphone penetration, expanded digital identity infrastructure, and evolving regulatory frameworks supporting open banking have collectively accelerated this transition, particularly in high-growth markets across Asia Pacific, Latin America, and Sub-Saharan Africa. North America currently leads the market in revenue contribution, while Asia Pacific is positioned as the fastest-growing region over the forecast period.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

A personal loan is an unsecured financial instrument extended by banks, credit unions, digital lenders, or peer-to-peer platforms to individual borrowers for a wide range of personal expenditure needs. Unlike mortgage loans or vehicle financing, personal loans are not tied to a specific asset and do not require collateral from the borrower. The approved loan amount, repayment tenure, and interest rate are primarily determined by the borrower's creditworthiness, income profile, employment history, and existing debt obligations.

The personal loan market encompasses all financial activities related to the origination, servicing, securitization, and distribution of these credit instruments. Loan purposes are diverse, spanning debt consolidation, home renovation, medical expenses, educational costs, travel, wedding financing, and emergency liquidity needs. Lenders range from full-service commercial banks and regional credit unions to specialized non-bank financial companies (NBFCs), fintech platforms, marketplace lenders, and peer-to-peer networks that connect retail investors directly with individual borrowers.

The market operates within regulatory frameworks defined by central banks, financial services authorities, and consumer credit regulators, with rules governing interest rate disclosure, lending eligibility criteria, and debt collection practices varying significantly across geographies. Regulatory evolution, including open banking mandates, digital identity frameworks, and borrower protection guidelines, is continuously reshaping both market access and competitive dynamics within the personal lending industry.

The personal loan industry is in the middle of a structural shift. Fintech originators are pulling market share from traditional banks, AI driven underwriting is rewriting how credit decisions get made, and big asset managers are pouring capital into loan platform partnerships to back the next leg of growth. None of this is theoretical anymore. The numbers and deal flow over the past 18 months make it clear that the lending model is changing fast.

In March 2026, SoFi Technologies announced over USD 3.6 billion in new personal loan delivery commitments across three partnerships, including a USD 1 billion deal with a leading global bank and a USD 2 billion two-year tie-up with a top-five private asset manager, extending its capital-light fee-based revenue strategy.

In February 2026, LendingClub outlined plans to expand its personal lending franchise, roll out a new home improvement financing product, and continue a USD 100 million share repurchase and acquisition programme initiated in November 2025, signalling a sharper focus on broadening its consumer loan mix and earnings visibility.

On 18 June 2025, LendingClub Bank launched LevelUp Checking, offering personal loan borrowers 2% cash back on monthly loan payments made through the account. The product bundles checking and lending to deepen member retention and drive product cross-sell across its digital banking base.

On 17 April 2025, SoFi Technologies announced a USD 3.2 billion expansion of its Loan Platform Business, including a USD 2 billion extension with Fortress Investment Group for personal loans and a USD 1.2 billion two-year originations agreement with a Fortress and Edge Focus joint venture, lifting Fortress's total commitment to over USD 5 billion.

AI underwriting, big data analytics, and chatbots are now central to lender competitiveness. Platforms like Upstart use over 1,600 alternative data points to approve borrowers traditional models reject, accelerating personal loan market growth as fintechs originate close to half of new account balances in the United States.

P2P platforms strip out the traditional intermediary, deliver higher returns for investors, and pass lower interest rates to borrowers. Zopa in the UK and LendingClub in the US remain reference cases, and the personal loan market trends point to deeper P2P penetration across both prime and near-prime segments.

Schemes such as India's Pradhan Mantri Jan Dhan Yojana have brought tens of millions of new borrowers into the formal credit system, creating a structural pull for short-term personal financing. The personal loan industry growth in South Asia and Southeast Asia is increasingly tied to this inclusion led demand base.

Private capital is anchoring the next phase of consumer lending. SoFi's USD 5 billion-plus partnership with Fortress and Blue Owl Capital, announced through 2024 and 2025, exemplifies how asset managers are providing balance sheet capacity for fintech lenders, directly accelerating the personal loan market growth.

Market players are stitching together loans, checking, and rewards to lift retention and lifetime value. LendingClub's June 2025 LevelUp Checking launch, which pays 2% cash back on personal loan payments, is a tangible example of how product bundling is becoming a defining feature of the personal loan industry.

Consumer preference for unsecured personal loans has expanded significantly as household expenditure patterns diversify and financial needs become more varied. Medical emergencies, home improvement projects, education financing, and lifestyle spending have positioned personal loans as the preferred short-to-medium-term borrowing instrument for working adults across income tiers. The removal of collateral requirements reduces application friction and accelerates approval cycles, directly addressing the time-sensitive nature of many consumer financing needs. As income levels rise across emerging economies and urban consumers build stronger credit histories, the addressable market for personal loans continues to widen, with lenders extending credit to segments previously excluded from the formal financial system.

The digitalization of lending workflows represents one of the most consequential drivers of market expansion. End-to-end digital origination platforms, supported by automated KYC processes, digital income verification, and real-time bank statement analysis, have compressed loan approval timelines from weeks to minutes. Mobile-first lender interfaces have made personal loans accessible to a generation of consumers who conduct financial transactions predominantly through smartphones. The cost savings generated by digital automation have enabled lenders to profitably serve smaller loan sizes and lower income tiers, unlocking new customer segments. Investment in cloud-native lending infrastructure, API-based credit bureau integrations, and open banking data feeds continues to accelerate across all major markets.

Fintech companies have fundamentally disrupted personal lending by deploying alternative data sources in credit assessment models. Behavioral data, transaction histories, utility payment records, psychometric scores, and mobile usage patterns supplement or replace traditional credit bureau data, particularly in markets with limited bureau penetration. Machine learning-based underwriting engines deliver more accurate risk stratification than conventional scorecard models, reducing default rates while extending credit to underserved populations. This innovation layer is driving broader financial inclusion and enabling market growth in regions where traditional credit infrastructure remains underdeveloped. The increasing sophistication of these models is also reducing time-to-decision for borrowers, improving conversion rates across digital lending channels.

Regulatory mandates and market forces are converging to accelerate financial inclusion, particularly in South and Southeast Asia, Sub-Saharan Africa, and Latin America. Governments across these regions have implemented digital public infrastructure, including biometric identity systems, real-time payment rails, and open banking frameworks that lower the cost of borrower onboarding. Rising smartphone penetration combined with expanding mobile internet coverage has extended the reach of digital lending platforms to rural and semi-urban populations previously excluded from the formal credit ecosystem. Development finance institutions and microfinance networks are also channeling capital into personal lending infrastructure, creating enabling conditions for sustained market growth in underserved geographies.

Artificial intelligence is transforming credit risk assessment across the personal loan market. Machine learning models trained on large historical loan portfolios now deliver credit decisions with higher accuracy and lower turnaround times compared to traditional underwriting approaches. Real-time fraud detection algorithms analyze behavioral biometrics, device fingerprints, and transaction patterns to identify synthetic identity fraud and application manipulation before disbursement. Generative AI tools are beginning to streamline loan officer workflows, summarize borrower documentation, and flag credit exceptions for human review, combining automation speed with contextual judgment. The adoption of explainable AI frameworks is also improving regulatory acceptance of algorithmic credit decisions in jurisdictions with consumer fairness requirements.

Personal loans are increasingly being distributed through non-financial platforms rather than standalone lending applications. E-commerce marketplaces, healthcare networks, travel booking platforms, salary management apps, and gig economy tools are integrating personal loan products directly into their workflows, capturing borrower intent at the point of need. This embedded finance model reduces customer acquisition costs for lenders, increases conversion rates, and creates differentiated borrower relationships anchored in existing platform engagement. Partnerships between licensed lenders and technology platforms are accelerating, with major technology companies entering financial services through loan facilitation, credit marketplaces, and co-branded lending products.

The funding model for personal loans has diversified significantly with the growth of asset-backed securitization and private credit markets. Fintech lenders originate personal loans and package them into rated securities distributed to institutional investors, creating a capital-efficient originate-to-distribute model that reduces balance sheet concentration. Asset managers, pension funds, and insurance companies seeking yield have increased allocations to consumer asset-backed securities, providing durable capital to support personal loan market growth. This capital market integration has reduced funding costs for leading originators and supported more competitive interest rate pricing for borrowers. Private credit agreements between fintech platforms and institutional investors have also become a primary growth-financing mechanism for mid-size lending platforms.

RegTech solutions are enabling lenders to manage compliance obligations more efficiently across multi-jurisdictional lending operations. Automated consumer credit disclosure generation, real-time interest rate monitoring, borrower consent management, and machine-readable regulatory reporting reduce the compliance burden that has historically limited the scalability of smaller lending platforms. Open banking mandates in the United Kingdom, digital lending guidelines in India, and account aggregation regulations across Southeast Asia have created standardized data-sharing environments that streamline income verification and credit assessment without increasing manual processing costs. Lenders investing in compliance automation are achieving faster market entry timelines and lower per-loan regulatory costs relative to incumbents relying on manual compliance workflows.

The personal loan market faces persistent challenges centered on credit risk management and portfolio quality in a dynamic economic environment. As lenders expand origination volumes into new borrower segments with thinner credit histories, delinquency and default rates carry heightened sensitivity to macroeconomic fluctuations including employment contraction, inflationary pressure on household budgets, and interest rate volatility. Digital lending platforms face elevated exposure to application fraud and synthetic identity schemes, demanding continuous investment in fraud detection and borrower verification infrastructure. The growing reliance on alternative data in underwriting, while broadening credit access, introduces model risk and interpretability challenges that regulators are scrutinizing more closely across North America, Europe, and Asia Pacific. Lenders must balance the speed and inclusivity benefits of AI-driven credit decisions against the governance and fairness requirements imposed by evolving regulatory frameworks.

Regulatory complexity represents a structural restraint on market expansion, particularly for cross-border and digital-first lending operations. Divergent consumer credit laws, interest rate disclosure requirements, data localization mandates, and licensing frameworks across jurisdictions increase operational costs and limit scalability for lenders seeking to grow across multiple markets simultaneously. Tightening capital adequacy requirements for bank-originated consumer credit are leading some traditional institutions to reduce unsecured personal loan origination volumes or redirect capital to lower-risk secured asset classes. Rising funding costs in higher interest rate environments compress net interest margins for lenders operating asset-heavy balance sheet models, constraining portfolio growth rates and increasing pricing pressure on loan terms. Regulatory uncertainty around algorithmic underwriting and AI-based credit decisioning is also creating compliance risk that slows technology adoption in more conservative lending institutions.

Despite these headwinds, the personal loan market presents substantial long-term opportunities for well-positioned participants. The approximately 1.4 billion unbanked and underbanked adults globally represent a significant untapped credit market accessible through mobile-first, alternative data-driven lending models operating at lower cost than traditional branch-based origination. Green personal loans tied to energy-efficient home improvements, electric vehicle purchases, and solar installations represent an emerging product category with strong regulatory tailwinds and growing consumer demand across developed markets. Strategic partnerships between fintech originators and institutional capital providers create capital-efficient growth pathways that reduce balance sheet constraints on origination volume. Advances in explainable AI are progressively reducing regulatory friction around algorithmic credit decisions, enabling faster deployment of technology-driven underwriting models. Stakeholders seeking to understand these opportunity vectors in granular detail across regions, segments, and competitive positioning are invited to explore the full Expert Market Research report for comprehensive analysis.

The Expert Market Research Personal Loan Market report provides detailed segmentation analysis across loan type, lender type, loan purpose, loan tenure, and region. The segmentation framework captures the full diversity of the personal lending market and identifies the highest-growth pockets within the overall forecast.

Market Breakup by Type

Key Insight: P2P marketplace lending continues to claim share by skipping the traditional bank middleman, which translates into better returns for investors and cheaper credit for borrowers. Balance sheet lending still anchors the volume base, however, with banks and finance companies retaining loans on their own books and offering greater transparency in pricing and servicing. The interesting structural shift over the forecast period is the rise of hybrid models, where fintechs originate loans and large asset managers absorb the credit risk through committed funding partnerships. SoFi's expanded loan platform business is the clearest example of this funding architecture in action across the personal loan market.

Market Breakup by Age

Key Insight: The 30 to 50 age band drives the bulk of personal loan volume, reflecting peak life-stage expenses, home improvements, debt consolidation, and family-related purchases. Borrowers under 30 represent the fastest-growing pocket of demand, fuelled by improved financial literacy, digital-first borrowing habits, and rising aspirations among urban millennials and Gen Z consumers. The over-50 segment remains stable, with personal loans typically used for medical needs, household upgrades, or supporting family financial goals. Across all three groups, rapid digital approval and collateral-free credit are reshaping where and how consumers transact in the personal loan industry.

Market Breakup by Marital Status

Key Insight: Married borrowers account for a sizable share of personal loan demand, drawn by household-level financial needs such as home renovations, child education, weddings, and large consumer durables. Single borrowers, while smaller in aggregate share, are scaling faster, fuelled by independent lifestyle choices, travel-led spending, and the rising acceptability of credit-funded experiences among urban professionals. Lenders are increasingly customising loan tenures and EMI structures around these distinct life-stage profiles, supporting steady personal loan market growth across both groups.

Market Breakup by Employment Status

Key Insight: Salaried individuals dominate the personal loan market thanks to predictable income streams, cleaner credit histories, and faster underwriting outcomes. They remain the preferred segment for lenders, and the rise of AI-led credit scoring is widening access for first-time salaried borrowers in emerging markets. The business segment is set to grow faster, lifted by SME credit demand, working capital needs, and digital lending platforms purpose-built for self-employed borrowers. Alternative lending channels including P2P platforms and crowdfunding are particularly active in plugging financing gaps for this group.

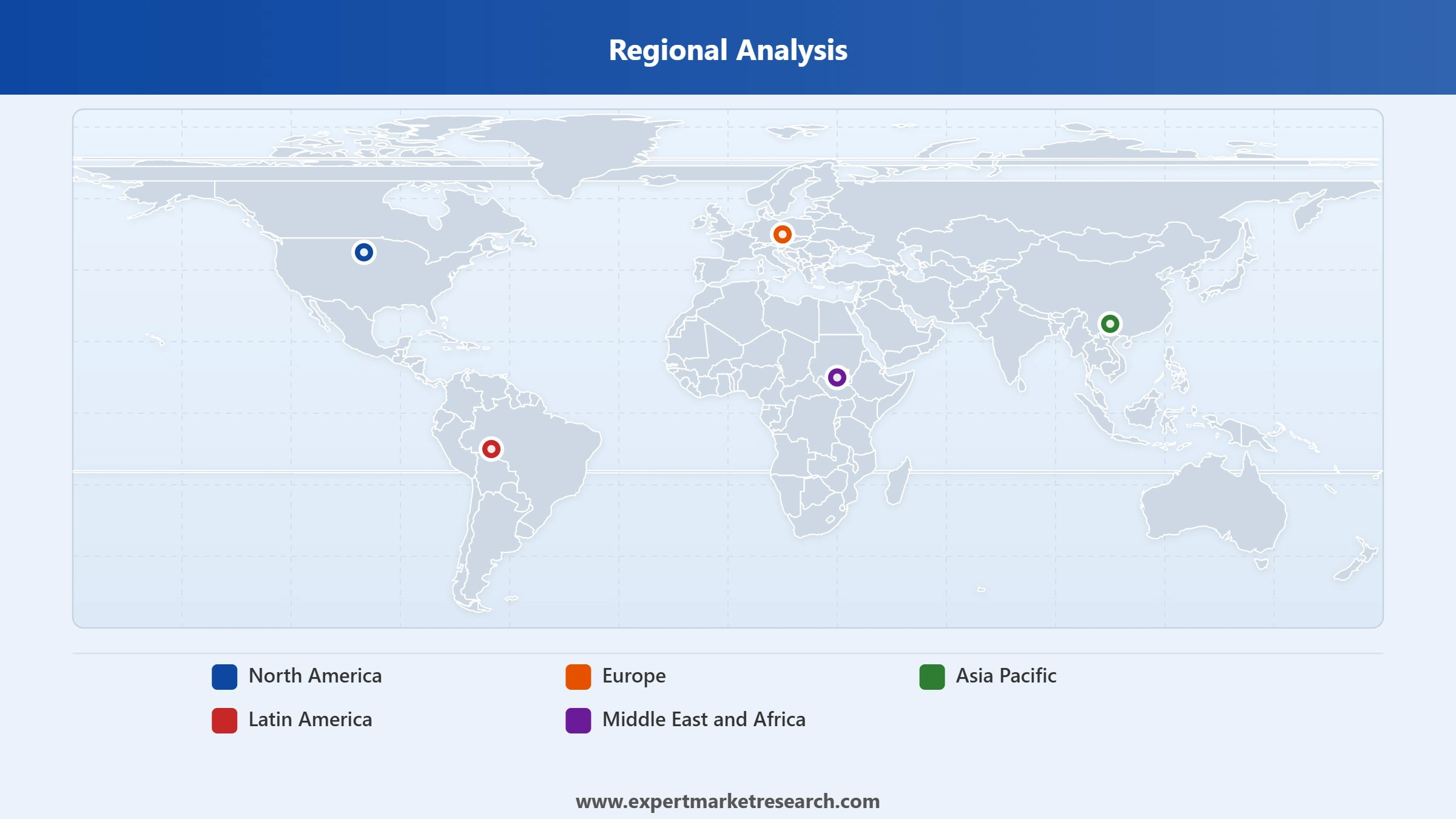

Market Breakup by Region

Key Insight: North America leads on growth velocity, with fintech-originated personal loans now accounting for nearly half of new account balances and total US unsecured balances crossing USD 253 billion by Q1 2025. Asia Pacific contributes the largest volumes by user base, with India, China, and Southeast Asia driving demand through urbanisation, digital onboarding, and rising consumption aspirations. Europe is scaling steadily on the back of digital-first applications, particularly across the UK and Germany. Latin America and the Middle East and Africa remain smaller in absolute terms but are expanding rapidly as mobile penetration, fintech regulation, and consumer credit infrastructure mature in tandem.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

North America represents the most mature and largest revenue-generating region in the global personal loan market. The United States anchors this dominance, with total US unsecured consumer balances reflecting robust consumer credit demand and a well-developed financial services ecosystem. Online lenders and marketplace platforms now account for nearly half of all new personal loan originations in the United States, representing a decisive structural shift from branch-based banking toward platform-enabled credit access. A sophisticated credit bureau network, high consumer financial literacy, and strong regulatory clarity around consumer lending have collectively created favorable conditions for market growth. North America is projected to expand at a CAGR of approximately 37.1% over the forecast period, the highest growth rate of any region, as fintech lenders capture rising share of new account balances. Canada follows with strong digital banking adoption, while Mexico shows accelerating growth driven by financial inclusion initiatives targeting the large unbanked population.

Europe is the second-largest regional market, characterized by progressive digital finance regulation and a heterogeneous banking landscape across member states. The United Kingdom and Germany represent the largest national markets, supported by mature credit infrastructure, high digital banking penetration, and strong regulatory frameworks governing consumer credit transparency. The European Union's open banking directives have accelerated data sharing between incumbents and challengers, enabling fintech lenders to compete more effectively for personal loan originations across the EU28 geography. Spain, Italy, and France are showing improving growth momentum as improving labor market conditions support consumer borrowing confidence. Green lending products are gaining market share in Scandinavia and Western Europe, tied to energy retrofit financing and EV purchase loans. The UK personal loans market continues to benefit from a competitive digital challenger bank ecosystem and a well-established marketplace lending infrastructure.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Asia Pacific is the fastest-growing regional market in the global personal loan landscape, driven by demographic scale, rapid urbanization, and accelerating smartphone-enabled financial services adoption. India represents one of the largest national markets by borrower volume, with a maturing digital lending ecosystem supported by account aggregator frameworks, the Unified Payments Interface, and expanding credit bureau coverage in urban and semi-urban markets. China's personal loan market is anchored by technology-enabled consumer finance platforms that serve a vast and digitally sophisticated borrowing population. Japan and South Korea represent high-income, digitally mature markets with stable personal loan demand from salaried workers and small business owners. Southeast Asian markets including Indonesia, Vietnam, and the Philippines are experiencing high growth from digital lending platforms targeting the underbanked population, supported by improving smartphone penetration rates and mobile internet coverage.

Latin America is an emerging growth market for personal loans, with Brazil and Mexico representing the primary revenue contributors. Historically high inflation rates constrained personal loan market development in the region, but improving macroeconomic conditions, fintech proliferation, and expanding digital payment infrastructure are creating more favorable lending environments. Brazil's large underbanked population and growing fintech regulatory framework are attracting significant investment from domestic and international digital lending operators. Mexico is benefiting from financial inclusion programs and proximity to the United States-based venture capital ecosystem that supports fintech innovation. Regional lenders are adapting products to address the specific financial needs and income volatility patterns of Latin American borrowers, including income-linked repayment structures and digitally disbursed microloans.

The Middle East and Africa region is at an early stage of personal loan market development but offers substantial long-term growth potential. GCC countries including Saudi Arabia, the UAE, and Kuwait are characterized by relatively high per-capita incomes, sophisticated banking sectors, and a young, digitally connected population creating favorable conditions for premium personal loan products. South Africa represents the most developed personal lending market on the continent, with a well-established banking system and consumer credit framework. Sub-Saharan Africa presents a large mobile-first consumer base with limited access to traditional banking, creating strong demand for digitally delivered credit products. Financial inclusion mandates from governments and development finance institutions are channeling investment into digital lending infrastructure across Kenya, Nigeria, Ghana, and Egypt, creating conditions for sustained market growth over the forecast period.

The personal loan market features a layered competitive structure. At the top, global banks and credit card incumbents such as American Express, Wells Fargo, Goldman Sachs, and DBS leverage deep deposit bases and brand trust to anchor traditional lending volume. Alongside them, a powerful set of digital-first lenders including SoFi, LendingClub, Avant, and Prosper has built significant share by combining algorithmic underwriting, app-native onboarding, and partnership-led funding models.

Competition is shifting away from pure interest rate plays toward product bundling, partnership funding, and AI driven personalisation. Asset manager capital from firms such as Fortress and Blue Owl is flowing into fintech loan platforms at scale, while traditional banks are responding with technology investments and partnership models of their own. The next phase of the personal loan industry will likely be defined by which lenders can combine cost-efficient funding with genuinely differentiated borrower experiences.

Founded in 1850 and headquartered in New York, American Express is one of the world's largest financial services corporations and a major issuer of personal, small business, and corporate credit. The company offers personal loans, travel cards, freight forwarding, and digital banking products to a globally distributed customer base. Its strength in premium card holders translates into a high quality pool of pre-qualified borrowers for its personal lending business.

Established in 2012 and based in Illinois, United States, Avant is a leading financial technology firm focused on debt consolidation loans, emergency loans, home improvement loans, and instalment loans. The company targets prime and near-prime borrowers with competitive rates and a digital-first application experience, leveraging proprietary credit modelling to widen access for under-served segments of the personal loan market.

Founded in 1968 and headquartered in Singapore's Marina Bay district, DBS Bank Limited offers personal banking, credit cards, wealth management, corporate banking, and SME banking. The bank is widely recognised for its digital banking leadership across Asia, with smart, app-native lending journeys that have made it a benchmark for digital personal loan origination across Singapore, Hong Kong, India, Indonesia, and other key Asia Pacific markets.

Founded in 1869 and headquartered in New York City, The Goldman Sachs Group operates across investment banking, securities underwriting, asset management, wealth management, and private equity. Through Goldman Sachs Alternatives, the firm has also become an active funder of consumer credit innovation, including a USD 60 million Series C investment in fintech Kashable in 2025 to support employer-facilitated personal loans across the United States.

Other key players in the market are LendingClub Bank, N.A., Prosper Funding LLC., SoFi Lending Corp., Truist Financial Corporation, Wells Fargo & Company, Industrial and Commercial Bank of China Limited, and Others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Get the latest perspective on the personal loan market with our 2026 report. Track the rise of fintech-led origination, the funding partnerships fuelling the next leg of growth, and the segment-level shifts reshaping demand across regions. Whether you are a bank planning a digital lending overhaul, an asset manager evaluating consumer credit allocations, or a fintech building product depth, the report delivers the clarity you need. Download your free sample now and explore the opportunities reshaping the thriving personal loan industry.

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

The market is projected to grow at a CAGR of 32.20% between 2026 and 2035.

The advantages offered by personal loans, increasing requirement of money to fund lifestyle upgrades, and increasing accessibility of personal loans are major drivers of the market.

Key trends aiding market expansion include the technological advancements within market, adoption of digital technologies, rising expenditure on luxury goods, government initiatives promoting financial inclusion, and increasing immigration towards urban cities.

Regions considered in the market are North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa.

P2P marketplace lending and balance sheet lending are the different types of personal loans.

Less than 30 years, 30-50 years, and more than 50 years of age groups are considered in the market.

Based on marital status, the market is segmented into married and single.

A personal loan can be taken from an online lender, credit union, or a bank.

A personal loan is considered a good way of fulfilling short-term or long-term financial needs and an adequate amount of time is given for consolidation.

Key players in the market are American Express Company, Avant, LLC., DBS Bank Limited, The Goldman Sachs Group, Inc., LendingClub Bank, N.A., Prosper Funding LLC., SoFi Lending Corp., Truist Financial Corporation, Wells Fargo & Company, and Industrial and Commercial Bank of China Limited, among others.

In 2025, the market attained a value of nearly USD 354.96 Billion.

The market is estimated to witness a healthy growth in the forecast period of 2026-2035 to reach about USD 5787.54 Billion by 2035.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Age |

|

| Breakup by Marital Status |

|

| Breakup by Employment Status |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.