Consumer Insights

Uncover trends and behaviors shaping consumer choices today

Procurement Insights

Optimize your sourcing strategy with key market data

Industry Stats

Stay ahead with the latest trends and market analysis.

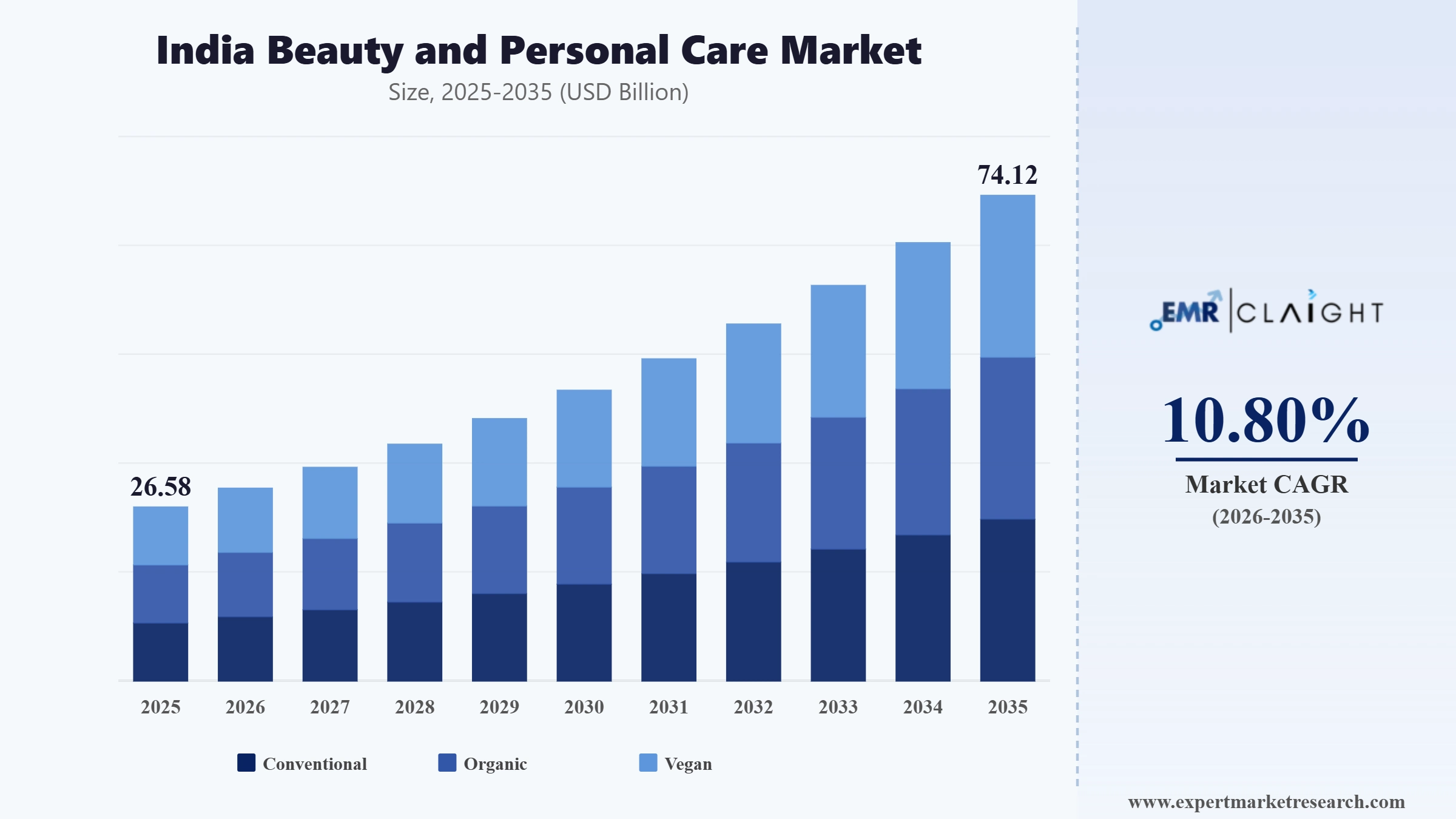

The India beauty and personal care market attained a value of USD 26.58 Billion in 2025 and is projected to expand at a CAGR of 10.80% through 2035. The market is further expected to achieve USD 74.12 Billion by 2035. Due to increased demand for customized skin solutions, premium beauty products, and more digitally-focused shopping experiences, there is pressure on beauty brands to innovate faster and develop new distribution channels as well as consumer engagement programs.

The India beauty and personal care market is witnessing a rise in consumer consciousness about preventive skincare and wellness-driven personal care products. At the same time, fast-growing organized retail and online beauty stores are facilitating greater access to products and helping brands enter under-penetrated markets.

One key trend in the market is the continuous growth of premium beauty products by companies like Hindustan Unilever through their acquisitions-based model and digital-first approach towards portfolio expansion. For example, in June 2026, L'Oréal acquired a majority stake in Indian beauty startup Innovist, adding digital-first brands such as Bare Anatomy and Chemist at Play to strengthen its presence in the India beauty and personal care market. Companies are focusing on building up their presence through brands in skincare, derma beauty, and premium cosmetics due to increasing demands from wealthier and digitally savvy consumers. Such an initiative is in line with the changing India beauty consumption scenario, where online sales of beauty and personal care are overtaking those of several offline categories. The rising popularity of beauty-driven online platforms along with growing consumer expenditure on specialized skincare and wellness products is compelling manufacturers to innovate quickly and launch premium products.

The India beauty and personal care market is also undergoing a structural change through premiumization of products, innovative ingredients, and technology-enabled consumer engagement. Manufacturers are increasingly focusing on scientific formulations, dermatologist-tested products, and customized products for Indian skin and climate. For example, in June 2024, Kosmoderma launched its Mumbai clinic featuring Soprano Titanium, Morpheus8, Forma, and HydraFacial technologies for advanced aesthetic treatments. Companies are also using artificial intelligence for beauty recommendations, virtual trials, and consumer analysis. Moreover, sustainability is becoming an important strategy for companies, which is leading to the introduction of refillable packages, biodegradable materials, and sustainably sourced ingredients.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Beautyverse 2026 was announced by Amazon that brought together beauty brands, celebrities, creators, and consumers through immersive experiences. Such campaigns offer chances for businesses to boost brand visibility, influencer marketing, and omnichannel customer acquisitions.

Paula’s Choice expanded its presence in India through Tira Beauty by making its scientific-based skin care products accessible. Such alliances help beauty brands tap into premium retail and fast-growing skincare consumer base, boosting the India beauty and personal care market value.

The British cosmetics company Lush opened its first flagship store in India at Nexus Select Citywalk, Delhi, and is offering its customers fresh and handmade products like Fresh Face Masks and Solid Shampoo Bars that are cruelty-free in nature. It is through such developments that cosmetic companies have an opportunity to offer sustainable products and meet the increasing demand for premium personal care items.

APR entered the Indian beauty market by launching Medicube on Nykaa, expanding access to Korean skincare innovations. Such advancements in the India beauty and personal care market encourage companies to capitalize on growing demand for K-beauty products through established digital retail channels.

The development of premium skincare and personal care products is another important driving factor of the India beauty and personal care market growth since more consumers are becoming interested in clinically proven and specialty products. Premium skincare and cosmetics are becoming an important focus area for leading manufacturers as they can help to achieve better profit margins and ensure brand loyalty among consumers. The demand for efficacy-driven products is especially high in the urban areas of India. In June 2026, Hindustan Unilever, for example, launched AI-powered fragrance hub in India, accelerating premium beauty innovation and development.

Beauty brands are increasingly using artificial intelligence and big data analytics to provide consumers with personalized experience, thereby reshaping the India beauty and personal care market dynamics. Advanced algorithms based on machine learning and data mining techniques are used to enhance conversion rate optimization and consumer retention. Beauty brands use online consumer engagement platforms to collect valuable insights from consumers and develop innovative products. For example, in June 2026, Fiabila launched its Smart Beauty concept in India, integrating advanced nail technologies, trend forecasting, and customized beauty solutions. Additionally, India's Digital India initiative increases digital connectivity across the country which creates favorable conditions for beauty brands.

Innovation towards sustainability is rapidly changing the landscape of the India beauty and personal care market. There is increased pressure on producers to develop innovative products that incorporate natural ingredients, ethical sources of production, and environmentally friendly packaging. As a result, companies introduce new refillable packages, eco-friendly packaging, and products which do not include controversial components. Sustainable product ranges are promoted by companies such as The Body Shop and Mamaearth. On the other hand, in April 2023, CavinKare introduced Truthsome, a digital-first clean beauty brand offering transparent, chemical-free haircare and skincare products across e-commerce channels.

The rise of beauty-focused digital marketplaces is creating great opportunities for the development of manufacturing companies and brands. The use of digital platforms helps companies reach consumers outside major urban centers, increasing visibility of the brands and their products, and making customer acquisition more effective. E-commerce leaders such as Nykaa and Purplle are expanding their ranges owing to special offers, collaborations with influencers and advanced merchandizing approaches. Thus, e-commerce makes it possible for startups to compete with international brands, accelerating the India beauty and personal care market value. Moreover, government programs aimed at promoting digital payments and development of e-commerce infrastructure contribute to further growth of online retail penetration in India. Consequently, in June 2026, Myntra Beauty introduced Seapuri and Frankly through Kindlife, strengthening its premium K-beauty portfolio and skincare offerings.

The increasing demand for beauty products inspired by Ayurveda principles is driving corporations towards developing formulas which use traditional herbs of India backed by scientific confirmation. Increasing consumer interest in beauty products using turmeric, neem, ashwagandha, saffron, and many other herbs which contribute to good health is being observed. Major brands are making investments in research and development to make their heritage ingredients commercially viable. For instance, brands such as Dabur and Himalaya Wellness are introducing advanced Ayurveda-based formulas for skin and hair care products for health-oriented clients. Aligning with this trend in the India beauty and personal care market, in June 2026, Reliance Retail introduced Puraveda on Tira, combining Ayurvedic ingredients with modern formulations to address rising demand for natural beauty and wellness products in India.

The Expert Market Research’s report titled “India Beauty and Personal Care Market Report and Forecast 2026-2035” offers a detailed analysis of the market based on the following segments:

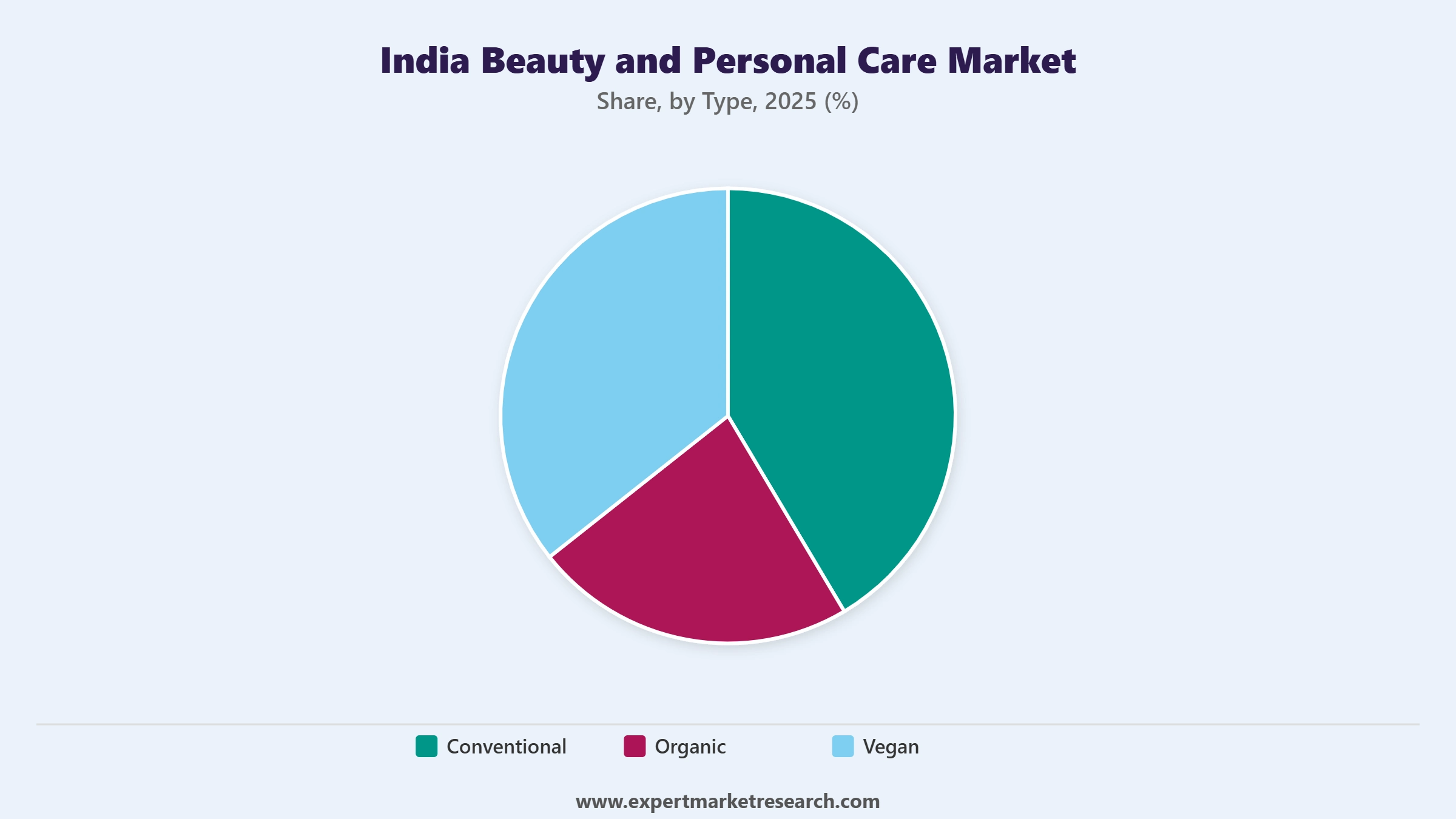

Market Breakup by Type

Key Insight: The type segmentation is influenced by the changing trends in the preferences of customers in the India beauty and personal care market. The conventional products continue to dominate the market on account of the trust of consumers, availability of a wide range of products, and affordability. Organic products continue to attract consumers who prefer products that are made using natural ingredients with minimal chemical content. In April 2025, KORA Organics re-entered the Indian market through Nykaa, expanding access to certified organic skincare products and strengthening the premium clean beauty segment. Vegan products are gaining momentum owing to the ethical purchase behavior, sustainability trends, and consumer education about the sources of ingredients.

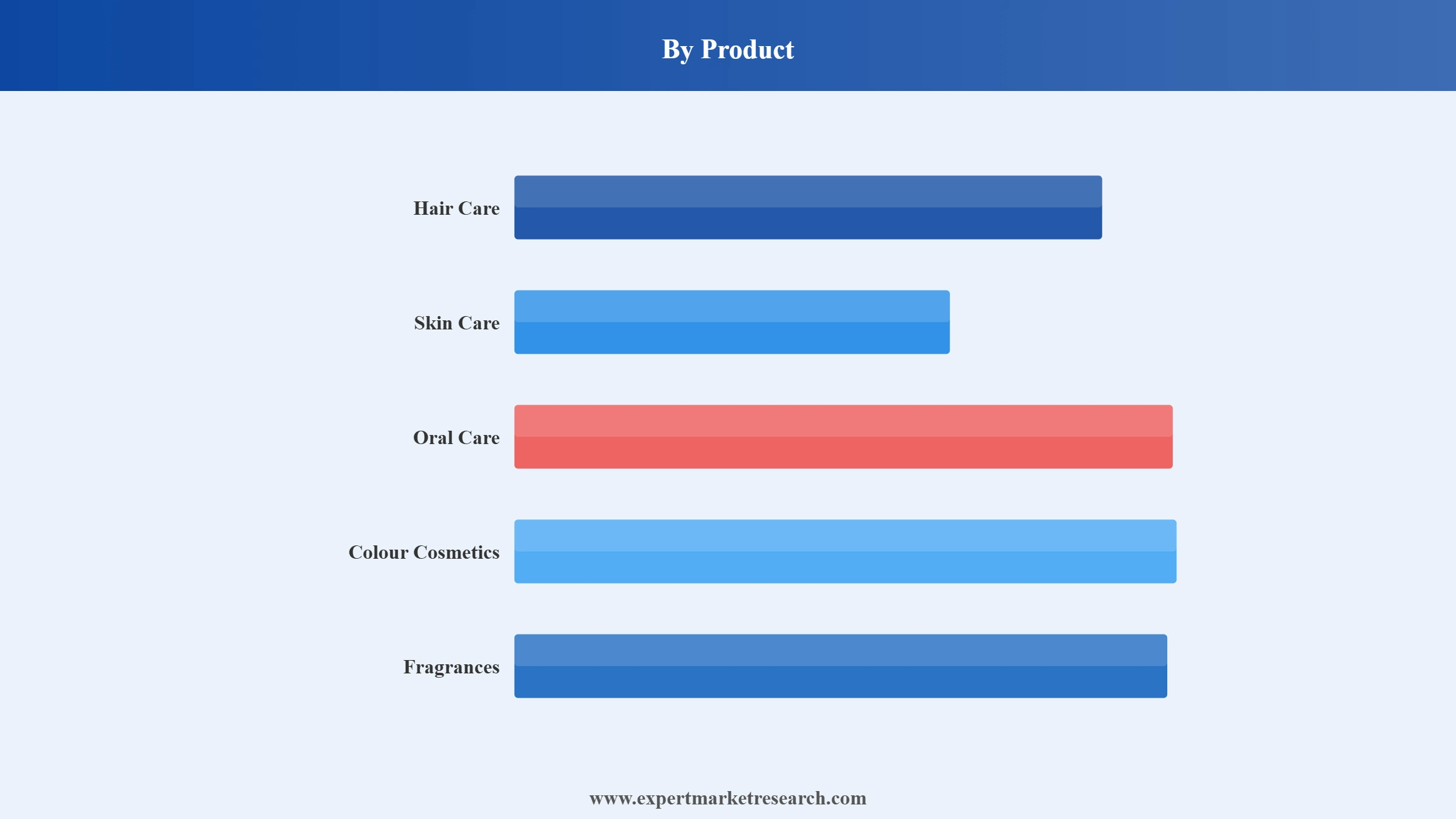

Market Breakup by Product

Key Insight: Product segmentation brings out various patterns of consumption in the India beauty and personal care market landscape. Skin care holds significant dominance owing to the growing focus on prevention, skin health, and personalized treatments. Hair care products are continuing to grow owing to hair and scalp health and pollution. In June 2025, Nexxus expanded into India with its premium haircare range, offering salon-grade, protein-focused formulations for advanced hair repair and nourishment. Oral cosmetics are growing owing to the heightened awareness around the importance of cosmetic oral hygiene. Color cosmetics are rapidly expanding its share considering trends in self-expression and online beauty. Fragrances are gaining popularity owing to the aspiration for premium lifestyles and gifting occasions.

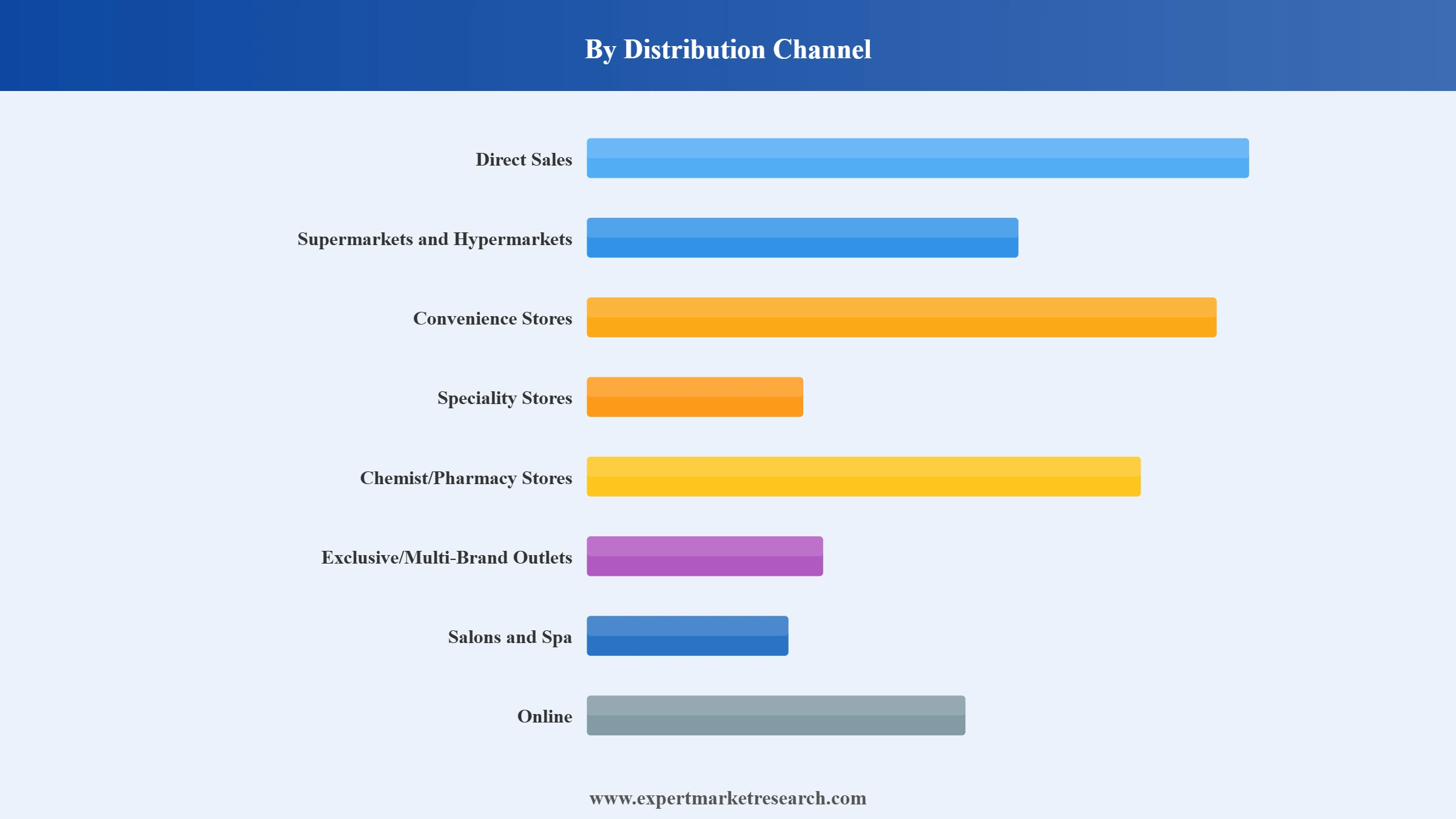

Market Breakup by Distribution Channel

Key Insight: The distribution channel structure is changing rapidly because of the omnichannel strategy that brands use in their development process. The key advantages of supermarkets and hypermarkets include accessibility, range of goods, and the high level of consumer trust. Convenience stores make it possible to buy essential personal care products frequently. Chemists and pharmacies benefit from the increasing number of therapeutic and dermatologist-endorsed products, accelerating the India beauty and personal care market value. Exclusive and multi-branded retail stores add value to the premium brands and increase consumer involvement. Salons and spas contribute to the market by making professional recommendations for products. In March 2026, Lush partnered with Myntra, expanding premium cruelty-free beauty products across India's digital consumers.

Market Breakup by Region

Key Insight: Performance of the overall India beauty and personal care market is subject to consumer tastes, economic development, and retail infrastructure. The regions of West and Central India dominate in the market by virtue of urban consumption and luxury product requirements. North India enjoys a high number of consumers and beauty consciousness among both metropolitan and emerging cities. East India is showing steady growth due to improved retail infrastructure and higher disposable incomes. Additionally, South India is showing rapid growth owing to health-consciousness among consumers and innovation in beauty products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

By type, conventional products register the largest share of the market due to widespread availability, strong brand trust, and extensive product portfolios

The conventional beauty and personal care items dominate the India beauty and personal care market dynamics due to their high consumer acceptance, wide reach, and affordable prices. Major manufacturers are leaders by virtue of their brand equity in skincare, haircare, oral care, and cosmetics. They enjoy the advantage of long years of consumer trust, constant innovations, and wide availability of their products via organized and unorganized retail outlets. The ability of these products to cater to the requirements of different income levels and regions is continuing to contribute to the leadership position of such products on the market.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Vegan beauty and personal care products are becoming one of the most rapidly developing segments in the India beauty and personal care market because of the growth of consumers' preferences for transparent and ethical consumption. Vegan brands are creating their formulations without animal-based components and are highlighting the sustainable nature of their products. Metropolitan consumers particularly pay more attention to sustainable items which match their personal values. Digital marketing techniques, endorsement by influencers, and increasing awareness about clean beauty facilitate the adoption of the aforementioned segment by consumers. In March 2026, Humuss Beauty launched its clean vegan skincare range in India, focusing on plant-based ingredients, sustainability, and conscious beauty formulations.

The skin care segment accounts for the largest share of the market due to growing preventive beauty routines and premium product adoption

Skin care captures the dominant share of the India beauty and personal care market revenue owing to growing emphasis on skin wellness, hydration, anti-aging and preventive beauty products. Manufacturers are introducing a variety of products catering to problems like skin pigmentation, skin breakouts, sensitivity and other problems specific to consumers of India. Increasing awareness about dermatological wellness and customized skin care regimes is resulting in increased usage of skin care products among all age groups. Trends related to premiumization are also leading consumers to choose special serums, sunscreens and skin care products, thus supporting the segment’s leadership in the entire beauty industry.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

The fastest growing segment is that of color cosmetics driven by changing preferences of consumers towards beauty and higher disposable incomes along with social media influenced trends related to beauty and makeup. Consumers are choosing makeup products according to different skin tones. In response, beauty companies are developing new formulations and long-lasting products in addition to introducing shades suitable to all skin types. Online portals offering beauty products and virtual makeup are further helping in increasing demand from premium and mass color cosmetic segments in the India beauty and personal care market. In February 2025, Cosnova Beauty partnered with Reliance Retail to introduce Essence in India, expanding access to affordable, trend-driven color cosmetics and strengthening the mass-premium beauty segment.

Supermarkets and hypermarkets secure the largest share of the market due to extensive product visibility and consumer trust

Supermarket and hypermarket channels retain their position of leading sales channels in the India beauty and personal care market on account of the availability of a broad assortment of products and credibility with the consumers. Shoppers are able to compare a range of products available along with price comparison and use promotions offered by each brand. Manufacturers can take advantage of shelf presence and high traffic to promote the products. The emergence of an increasing number of retail chains, especially organized retail chains in urban and semi-urban areas, positively affects sales performance through this channel.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

Online distribution channels experience rapid growth in the India beauty and personal care market since consumers become more willing to make online purchases. E-commerce portals provide customers with a range of benefits such as individualized recommendations, product description and review opportunities, and so forth. Beauty marketplaces are becoming popular because of high product availability in small cities and towns. Manufacturers use direct-to-consumer models of sales to increase engagement and obtain insights from consumers. Digital payments, better logistics, and marketing campaigns promote development of this distribution channel. For example, in December 2025, Naturals Salon unveiled its new direct-to-consumer (D2C) skincare brand, NXTFACE, aimed at catering to niche, younger segments of the population.

West and Central India clocks in the largest share of the market due to strong urban consumption and premium beauty adoption

The biggest regional market is represented by West and Central India as a result of higher levels of urbanization, better retailing infrastructure, and higher presence of beauty and personal care enthusiasts. Large metropolitan cities create demand for premium skincare products, cosmetics, and other personal care items through modern trade and digital platforms. This region is also an important center for manufacturing, distribution, and brand building efforts. Higher buying capacity, along with increased global beauty trends, makes consumers willing to try out more innovative products, making west and central parts of the country an important revenue earning region for the India beauty and personal care market players. In August 2025, Sugar Cosmetics partnered with Myntra to introduce a Gen Z-focused beauty brand, targeting younger consumers through trend-driven products.

Read more about this report - REQUEST FREE SAMPLE COPY IN PDF

South India emerges to be one of the fastest growing regional markets due to higher disposable incomes, expanding middle class, and increasing awareness about personal grooming and wellness. Consumers are becoming increasingly interested in premium skincare, hair care, and natural beauty products. The growth in organized retail and digital commerce is making it easier for brands to access South Indian consumers. In addition, the increasing demand for ingredient-based and wellness products is motivating manufacturers to expand the South India beauty and personal care market.

The sector is turning out to be more competitive with global and local players prioritizing premiumization, science-based formulations, beauty technology, and sustainable product development. Investments in AI-driven skin analysis, virtual beauty consultations, microbiome skincare, and ingredient transparency are the current strategies used by India beauty and personal care companies to increase consumer engagement. Key growth strategies include strategic acquisitions of digital native beauty brands and collaborations with dermatologists.

Expansion of direct-to-consumer distribution channels and penetration into Tier II and Tier III cities are some of the growth areas in the market. There is a huge potential for India beauty and personal care market players in vegan beauty, personalized skincare, Ayurveda-based formulations, and premium hair care products. Data analysis technologies are being used for faster product development and understanding emerging consumer preferences. The increasing importance of social commerce, beauty influencers, and e-beauty platforms provides customer acquisition opportunities for businesses.

Since its establishment in 1930 and being based in London, United Kingdom, Unilever supplies the India beauty and personal care industry through its subsidiary, Hindustan Unilever Limited. The company concentrates on premium skincare, haircare, and personal hygiene products while developing scientifically-proven beauty solutions. The strategy of the company is to engage consumers digitally, innovate in premium products, and acquire companies operating in fast-growing beauty segments in India.

Founded in 1837 and located in Cincinnati, Ohio, United States, Procter & Gamble operates in the market with its famous beauty and grooming brands. Product effectiveness, formulation technology, and consumer insights form the core of the company's activity while it keeps on developing its premium haircare and skincare portfolios by using data-driven marketing and omnichannel retail techniques in the India beauty and personal care market.

Founded in 1909 and headquartered in Clichy, France, L'Oréal is a pioneer in beauty technology and custom skincare solutions. This company appeals to Indian customers with its range of high-quality cosmetics, skincare, hair care, and professional beauty products. With an emphasis on beauty innovations driven by artificial intelligence, virtual consultations, dermatological experience, and sustainable development of products, L'Oréal manages to meet evolving customer demands and remain competitive.

Founded in 1882 and headquartered in Hamburg, Germany, Beiersdorf targets the Indian market with its globally renowned brands in skincare. This company specializes in dermatological innovation, skin health care, and premium skincare solutions meeting the needs of consumers. Through investment in clinically tested formulations and sustainability, as well as digital engagement channels, Beiersdorf supports its expanding presence in the India beauty and personal care market.

Other key players in the market include Revlon Inc., Kao Corporation, The Estée Lauder Companies Inc., Colgate-Palmolive Company, Godrej Group, Patanjali Ayurved Limited, Dabur India Ltd, and Johnson & Johnson Services, Inc., among others.

*Please note that this is only a partial list; the complete list of key players is available in the full report. Additionally, the list of key players can be customized to better suit your needs.*

Unlock the latest insights with our India beauty and personal care market trends 2026 report. Discover regional growth patterns, consumer preferences, and key industry players. Stay ahead of competition with trusted data and expert analysis. Download your free sample report today and drive informed decisions in the market.

India Beauty Salon Professional Market

Professional Beauty Services Market

India Beauty Supplements Market

India K-Beauty Products Market

India Clean Beauty Market

Upto 15% Off

USD

$2499 $2249

$3999 $3599

$4999 $4249

$5999 $5099

*While we strive to always give you current and accurate information, the numbers depicted on the website are indicative and may differ from the actual numbers in the main report. At Expert Market Research, we aim to bring you the latest insights and trends in the market. Using our analyses and forecasts, stakeholders can understand the market dynamics, navigate challenges, and capitalize on opportunities to make data-driven strategic decisions.*

In 2025, the India beauty and personal care market reached an approximate value of USD 26.58 Billion.

The market is projected to grow at a CAGR of 10.80% between 2026 and 2035.

Key strategies driving the market include ormulating adaptive products, partnering with salons and tech platforms, digitising inventory, and leveraging government schemes like PLI and PMKVY.

The key trends propelling the market are the increasing penetration of a wide range of brands and the growing popularity of herbal products.

The various types in the market are conventional, organic, and vegan.

Hair care, skin care, oral care, colour cosmetics, and fragrances, among others are the various products of beauty and personal care in the market.

The leading distribution channels in the market are direct sales, supermarkets and hypermarkets, convenience stores, specialty stores, chemist/pharmacy stores, exclusive/multi-brand outlets, salons and spa, and online, among others.

The major players in the market are Unilever plc, The Procter & Gamble Company, L'Oréal S.A., Beiersdorf AG, Revlon Inc., Kao Corporation, The Estée Lauder Companies Inc., Colgate-Palmolive Company, Godrej Group, Patanjali Ayurved Limited, Dabur India Ltd, and Johnson & Johnson Services, Inc., among others.

The market is estimated to witness healthy growth in the forecast period of 2026-2035 to reach a value of around USD 74.12 Billion by 2035.

The key challenges are formulation complexity, raw material inflation, regulatory ambiguities, and logistics fragmentation.

Explore our key highlights of the report and gain a concise overview of key findings, trends, and actionable insights that will empower your strategic decisions.

| REPORT FEATURES | DETAILS |

| Base Year | 2025 |

| Historical Period | 2019-2025 |

| Forecast Period | 2026-2035 |

| Scope of the Report |

Historical and Forecast Trends, Industry Drivers and Constraints, Historical and Forecast Market Analysis by Segment:

|

| Breakup by Type |

|

| Breakup by Product |

|

| Breakup by Distribution Channel |

|

| Breakup by Region |

|

| Market Dynamics |

|

| Trade Data Analysis |

|

| Competitive Landscape |

|

| Companies Covered |

|

Datasheet

One User

USD 2,499

USD 2,249

tax inclusive*

Single User License

One User

USD 3,999

USD 3,599

tax inclusive*

Five User License

Five User

USD 4,999

USD 4,249

tax inclusive*

Corporate License

Unlimited Users

USD 5,999

USD 5,099

tax inclusive*

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Small Business Bundle

Growth Bundle

Enterprise Bundle

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Flash Bundle

Number of Reports: 3

20%

tax inclusive*

Small Business Bundle

Number of Reports: 5

25%

tax inclusive*

Growth Bundle

Number of Reports: 8

30%

tax inclusive*

Enterprise Bundle

Number of Reports: 10

35%

tax inclusive*

How To Order

Select License Type

Choose the right license for your needs and access rights.

Click on ‘Buy Now’

Add the report to your cart with one click and proceed to register.

Select Mode of Payment

Choose a payment option for a secure checkout. You will be redirected accordingly.

Strategic Solutions for Informed Decision-Making

Gain insights to stay ahead and seize opportunities.

Get insights & trends for a competitive edge.

Track prices with detailed trend reports.

Analyse trade data for supply chain insights.

Leverage cost reports for smart savings

Enhance supply chain with partnerships.

Connect For More Information

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

Our expert team of analysts will offer full support and resolve any queries regarding the report, before and after the purchase.

We employ meticulous research methods, blending advanced analytics and expert insights to deliver accurate, actionable industry intelligence, staying ahead of competitors.

Our skilled analysts offer unparalleled competitive advantage with detailed insights on current and emerging markets, ensuring your strategic edge.

We offer an in-depth yet simplified presentation of industry insights and analysis to meet your specific requirements effectively.